QUESTION

We will discuss the Bayern Brauerei case. Should BB’s board of directors accept or reject the “project” which is expansion into Eastern Lander? You should base your decision on a NPV analysis of the project. In your memo, be sure to do the following:

– Evaluate and critique Max’s financial plan by expanding Exhibit 5 into a full-blown NPV analysis along the lines of what we did for the Brown-Forman case. Seven of ten rubrics deal with this issue.

– You will need to create a ten-year cash-flow forecast for 1993-2002 from the very limited information presented for 1989-1994

-You will need to include any incremental cash flows omitted by Max Leiter in Exhibit 5.

– You will need to estimate a discount rate for the project based upon very limited information.

– Identify and evaluate the biggest risk to which this project will expose BB. One rubric deals with this issue.

– Evaluate and critique the proposed compensation plan for Max by developing an alternative compensation scheme to the one proposed. One rubric deals with this issue.

– Evaluate and critique the proposal to increase the dividend paid out to shareholders and propose an alternative dividend policy. One rubric deals with this issue.

Model Fact

| This spreadsheet supports student analysis of the case, “Bayern Brauerei” (UVA -F-1027 v. 2.2). | ||

| Please note: | ||

| 1) This is a working model. Assumptions / Inputs presented can be changed to vary the results. | ||

| 2) This model intentionally incorporates a circular reference in its logic. In order to resolve this circularity, please instruct Excel to “iterate” 20 or so times in recalculating the model. This may be done by clicking on Tools/Options/Calculation, and then on Iteration. | ||

| 3) As long as default spreadsheet calculation is set as “automatic” impact of changing assumptions will be computed in real time. Alternatively F9 function key may need to be invoked to recalculate | ||

| results. To set numerical calculation settings to automatic look under tools, options, calculations menu. | ||

Revised: May 29, 1998

Copyright (C) 1998 by the Trustees of the University of Virginia Darden School Foundation.

Assumption

| Exhibit 1 | ||||||||

| Bayern Brauerei | ||||||||

| Forecast Assumptions | ||||||||

| Assumptions | Years | (Actual) | (Actual) | (Proj’d) | (Proj’d) | |||

| Sales Growth: Eastern Germany | 312.00% | 47.20% | 45.00% | 30.00% | ||||

| Sales Growth: Western Germany | 2.50% | 3.11% | 3.00% | 3.00% | ||||

| Operating Margin: East | 6.20% | 6.10% | 7.00% | 7.00% | ||||

| Operating Margin: West | 6.20% | 6.10% | 7.00% | 7.00% | ||||

| Capital Expenditures/Sales | 0.05 | 7 | ||||||

| Depreciation to Gross PPE | 0.10 | |||||||

| Dividend Payout | 0.75 | |||||||

| Melded Interest Rate | 0.11 | |||||||

| Average Tax Rate | 0.35 | |||||||

| Cash to Sales | 0.12 | |||||||

| Days Sales Outstanding: | ||||||||

| Eastern Germany | 90 | |||||||

| Western Germany | 41 | |||||||

| Allowance for Doubtful Accounts | ||||||||

| as a % of Accts. Rec. | 0.02 | |||||||

| Payables to Sales | 0.05 | |||||||

| Inventories to Sales | 0.14 | |||||||

| Other Current Assets to Sales | 0.1 | |||||||

| Other Current Liabs. to Sales | 0.11 | |||||||

Exhibit

BAYERN BRAUEREI

Historical and Projected Income Statements

Fiscal Year Ended December 31,

| 1989 | 1990 | 1991 | 1992 | 1993 | 1994 | ||

| (Actual) | (Actual) | (Actual) | (Actual) | (Proj’d) | (Proj’d) | ||

| 1 | Sales: Western Germany | 78,202 | 78,984 | 80,959 | 83,476 | 85,981 | 88,560 |

| 2 | Sales: Eastern Germany | – | 3,113 | 12,825 | 18,879 | 27,375 | 35,587 |

| 3 | Net Sales | 78,202 | 82,097 | 93,784 | 102,356 | 113,355 | 124,147 |

| Operating Expenses: | |||||||

| 4 | Production Costs and Expenses | 40,667 | 43,390 | 50,159 | 56,298 | 64,302 | 69,272 |

| 5 | Admin. and Selling Expenses | 15,734 | 15,967 | 18,663 | 20,164 | 21,000 | 24,000 |

| 6 | Depreciation | 4,550 | 5,439 | 7,367 | 7,650 | 7,650 | 8,530 |

| 7 | Excise duties | 11,526 | 11,174 | 11,734 | 11,949 | 12,469 | 13,656 |

| 8 | Total Operating Expenses | (72,477) | (75,970) | (87,923) | (96,061) | (105,421) | (115,458) |

| 9 | Operating Margin | 5,725 | 6,127 | 5,861 | 6,294 | 7935 | 8689 |

| 10 | Allowance for Doubtful Accounts | (9) | (6) | (28) | (19) | (188) | (46) |

| 11 | Interest Expense | (841) | (778) | (2,260) | (2,085) | (2,406) | (2,679) |

| 12 | Earnings Before Taxes | 4,875 | 5,343 | 3,573 | 4,190 | 5,341 | 5,964 |

| 13 | Income Taxes | (1,647) | (1,845) | (1,412) | (1,634) | (1,869) | (2,087) |

| 14 | Net Earnings | 3,228 | 3,498 | 2,161 | 2,556 | 3,471 | 3,877 |

| Dividends on : | |||||||

| 15 | Dividends to All Common Shs | 2,428 | 2,628 | 1,622 | 1,917 | 2,604 | 2,908 |

| 16 | Retentions of Earnings | 800 | 870 | 539 | 639 | 868 | 969 |

Exhibit 1 -contd-

BAYERN BRAUEREI

Historical and Projected Balance Sheets

(fiscal year ended December 31; all figures in DM thousands)

| 1989 | 1990 | 1991 | 1992 | 1993 | 1994 | ||

| (Actual) | (Actual) | (Actual) | (Actual) | (Proj’d) | (Proj’d) | ||

| Assets | |||||||

| 1 | Cash | 6,764 | 10,040 | 11,254 | 12,283 | 13,603 | 14,898 |

| 2 | Accounts Receivable | ||||||

| Western Germany | 8,740 | 9,004 | 9,104 | 9,477 | 9,658 | 9,948 | |

| Eastern Germany | 0 | 310 | 2,987 | 4,505 | 6,750 | 8,775 | |

| Allowance for Doubtful Accounts | (87) | (93) | (121) | (140) | (328) | (374) | |

| 3 | Inventories | 7,732 | 7,853 | 8,965 | 14,330 | 15,870 | 17,381 |

| 4 | Total Current Assets | 23,149 | 27,114 | 32,189 | 40,454 | 45,552 | 50,627 |

| 5 | Investments & Other Assets | 3,911 | 3,913 | 3,918 | 3,914 | 3,000 | 3,000 |

| 6 | Gross Property Plant & Equipt. | 73,667 | 73,667 | 76,500 | 76,500 | 85,300 | 93,933 |

| 7 | Accumulated Depreciation | (29,505) | (34,944) | (42,311) | (49,961) | (57,611) | (66,141) |

| 8 | Net Property Plant & Equipt. | 44,162 | 38,723 | 34,189 | 26,539 | 27,689 | 27,792 |

| 9 | Total Assets | 71,222 | 69,750 | 70,296 | 70,908 | 76,242 | 81,419 |

| Liabilities and Stockholders’ Equity: | |||||||

| 10 | Bank Borrowings (Short Term) | 3,765 | 7,172 | 7,640 | 7,891 | 12,651 | 16,977 |

| 11 | Accounts Payable | 4,511 | 4,607 | 4,705 | 5,328 | 5,668 | 6,207 |

| 12 | Other Current Liabilities | 9,325 | 9,031 | 10,316 | 11,259 | 12,469 | 13,656 |

| 13 | Total Current Liabilities | 17,601 | 20,810 | 22,661 | 24,478 | 30,788 | 36,841 |

| 14 | Long Term Debt: Bank Borrowings | 20,306 | 14,755 | 12,911 | 11,066 | 9,222 | 7,378 |

| 15 | Shareholders’ Equity | 33,315 | 34,185 | 34,724 | 35,364 | 36,231 | 37,201 |

| 16 | Total Liabs. & Stkhldrs’ Eq. | 71,222 | 69,750 | 70,296 | 70,908 | 76,242 | 81,419 |

Exhibit 2

BAYERN BRAUEREI

Sources and Uses of Funds

(fiscal year ending December 31; all figures in DM thousands)

| 1989 | 1990 | 1991 | 1992 | 1993 | 1994 | ||

| (Actual) | (Actual) | (Actual) | (Actual) | (Proj’d) | (Proj’d) | ||

| Sources of Funds | |||||||

| 1 | Net Income | 3,498 | 2,161 | 2,556 | 3,471 | 3,877 | |

| 2 | Increases in Allowance for Doubtful Accts. | 6 | 28 | 19 | 188 | 46 | |

| 3 | Depreciation | 5,439 | 7,367 | 7,650 | 7,650 | 8,530 | |

| 4 | Increases in Short Term Debt | 3,407 | 468 | 251 | 4,761 | 4,326 | |

| 5 | Increases in Accounts Payable | 96 | 98 | 623 | 340 | 540 | |

| 6 | Increases in Other Current Liabilities | (294) | 1,286 | 943 | 1,210 | 1,187 | |

| 7 | Total Sources of Cash | 12,152 | 11,407 | 12,042 | 17,620 | 18,505 | |

| Uses of Funds | |||||||

| 8 | Dividend Payments | 2,628 | 1,622 | 1,917 | 2,604 | 2,908 | |

| 9 | Increases in Cash Balance | 3,276 | 1,214 | 1,029 | 1,320 | 1,295 | |

| 10 | Increases in Accts. Receivable (W. Ger.) | 264 | 100 | 373 | 181 | 290 | |

| 11 | Increases in Accts Receivable (E. Ger.) | 310 | 2,677 | 1,518 | 2,245 | 2,025 | |

| 12 | Increases in Inventories | 121 | 1,112 | 5,365 | 1,540 | 1,511 | |

| 13 | Increases in Other Assets | 2 | 5 | (4) | (914) | 0 | |

| 14 | Reductions in Long Term Debt | 5,551 | 1,844 | 1,844 | 1,844 | 1,844 | |

| 15 | Capital Expenditures | 0 | 2,833 | 0 | 8,800 | 8,633 | |

| 16 | Total Uses of Cash | 12,152 | 11,407 | 12,042 | 17,620 | 18,505 |

Exhibit 3

BAYERN BRAUEREI

Ratio Analyses of Historical and Projected Financial Statements

(fiscal year ended December 31; all figures in DM thousands)

| 1989 | 1990 | 1991 | 1992 | 1993 | 1994 | ||

| (Actual) | (Actual) | (Actual) | (Actual) | (Proj’d) | (Proj’d) | ||

| Profitability | |||||||

| 1 | Operating Profit Margin (%) | 7.3% | 7.5% | 6.2% | 6.1% | 7.0% | 7.0% |

| 2 | Average Tax Rate (%) | 33.8% | 34.5% | 39.5% | 39.0% | 35.0% | 35.0% |

| 3 | Return on Sales (%) | 4.1% | 4.3% | 2.3% | 2.5% | 3.1% | 3.1% |

| 4 | Return on Equity (%) | 9.7% | 10.2% | 6.2% | 7.2% | 9.6% | 10.4% |

| 5 | Return on Net Assets (%) | 6.5% | 7.1% | 6.9% | 7.5% | 8.9% | 9.2% |

| 6 | Return on Assets (%) | 4.5% | 5.0% | 3.1% | 3.6% | 4.6% | 4.8% |

| Leverage | |||||||

| 7 | Debt/Equity Ratio (%) | 72.3% | 64.1% | 59.2% | 53.6% | 60.4% | 65.5% |

| 8 | Debt/Total Capital (%) | 41.9% | 39.1% | 37.2% | 34.9% | 37.6% | 39.6% |

| 9 | EBIT/Interest (x) | 6.8 | 7.9 | 2.6 | 3.0 | 3.3 | 3.2 |

| Asset Utilization | |||||||

| 10 | Sales/Assets | 1.10 | 1.18 | 1.33 | 1.44 | 1.49 | 1.52 |

| 11 | Sales Growth Rate (%) | 4.0% | 5.0% | 14.2% | 9.1% | 10.7% | 9.5% |

| 12 | Assets Growth Rate (%) | 6.0% | -2.1% | 0.8% | 0.9% | 7.5% | 6.8% |

| 13 | Receivables Growth Rate (%): Germany | 4.0% | 6.6% | 29.8% | 15.6% | 17.4% | 14.1% |

| 14 | Receivables Growth Rate: Western Germany | 4.0% | 3.0% | 1.1% | 4.1% | 1.9% | 3.0% |

| 15 | Receivables Growth Rate: Eastern Germany | 0.0% | NMF | 863.5% | 50.8% | 49.8% | 30.0% |

| 16 | Days in Receivables: Germany | 40.8 | 41.4 | 47.1 | 49.9 | 52.8 | 55.0 |

| 17 | Days in Receivables: Western Germany | 40.8 | 41.6 | 41.0 | 41.4 | 41.0 | 41.0 |

| 18 | Days in Receivables: Eastern Germany | NMF | 36.3 | 85.0 | 87.1 | 90.0 | 90.0 |

| 19 | Payables to Sales | 5.8% | 5.6% | 5.0% | 5.2% | 5.0% | 5.0% |

| 20 | Inventories to Sales | 9.9% | 9.6% | 9.6% | 14.0% | 14.0% | 14.0% |

| Liquidity | |||||||

| 21 | Current Ratio | 1.32 | 1.30 | 1.42 | 1.65 | 1.48 | 1.37 |

| 22 | Quick Ratio | 0.88 | 0.93 | 1.02 | 1.07 | 0.96 | 0.90 |

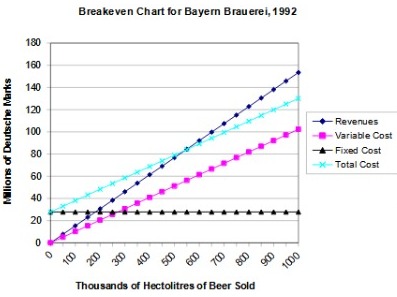

Exhibit 4

| Breakeven Analysis | ||||

| Fixed costs | 27,814 | |||

| Rev/Unit | 153.46 | |||

| VC/Unit | 102.29 | |||

| Breakeven | FC/Contrib | 543,607 | ||

| Change in WC/Unit | 59.76 | |||

| Volume | EBIT | |||

| 1 | Base | 667,000 | 6,313,496 | |

| 2 | 101% Volume | 673,670 | 6,654,771 | |

| 3 | Change | 6,670 | 341,275 | |

| 4 | % Change | 1.00% | 5.41% | |

| Operating Leverage = | 5.4 | |||

| Data for Profit Break-even Analysis Graph | ||||

| Volume | Revenues | Var. Cost | Fixed Cost | Tot. Cost |

| 0 | 0 | 0 | 28 | 28 |

| 50 | 8 | 5 | 28 | 33 |

| 100 | 15 | 10 | 28 | 38 |

| 150 | 23 | 15 | 28 | 43 |

| 200 | 31 | 20 | 28 | 48 |

| 250 | 38 | 26 | 28 | 53 |

| 300 | 46 | 31 | 28 | 59 |

| 350 | 54 | 36 | 28 | 64 |

| 400 | 61 | 41 | 28 | 69 |

| 450 | 69 | 46 | 28 | 74 |

| 500 | 77 | 51 | 28 | 79 |

| 550 | 84 | 56 | 28 | 84 |

| 600 | 92 | 61 | 28 | 89 |

| 650 | 100 | 66 | 28 | 94 |

| 700 | 107 | 72 | 28 | 99 |

| 750 | 115 | 77 | 28 | 105 |

| 800 | 123 | 82 | 28 | 110 |

| 850 | 130 | 87 | 28 | 115 |

| 900 | 138 | 92 | 28 | 120 |

| 950 | 146 | 97 | 28 | 125 |

| 1000 | 153 | 102 | 28 | 130 |

Exhibit 5

Max Leiter’s Analysis of the Return on Investment from

Investment in Accounts Receivable in the Eastern Lander

| Assumptions | |

| Revenue per HL (DM) | 153.46 |

| Variable Costs per HL (DM) | 102.35 |

| Contribution Percentage | 33% |

| Tax Rate | 35% |

| Sales in Eastern Lander (DM, thousands) | |

| Change in Sales (DM, thousands) | |

| Variable Costs on the Marginal Sales | |

| Contribution on the Marginal Sales | |

| Taxes on the Marginal Contribution | |

| Marginal After-tax Profits (DM thousands) | |

| Variable Costs/Sales | |

| Change in Accounts Receivable, Eastern Lander (DM thousands) | |

| Investment in Accts. Receivable (DM thousands) | |

| Return on Marginal Investment in Receivables |

| 1989 | 1990 | 1991 | 1992 | 1993 | 1994 | 1995 | 1996 | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 |

| (Actual) | (Actual) | (Actual) | (Actual) | (Proj’d) | (Proj’d) | (Proj’d) | (Proj’d) | (Proj’d) | (Proj’d) | (Proj’d) | (Proj’d) | (Proj’d) | (Proj’d) |

| – | 3,113 | 12,825 | 18,879 | 27,375 | 35,587 | ||||||||

| – | 3,113 | 9,712 | 6,054 | 8,496 | 8,212 | ||||||||

| – | (2,076) | (6,478) | (4,037) | (5,666) | (5,477) | ||||||||

| – | 1,037 | 3,235 | 2,016 | 2,829 | 2,735 | ||||||||

| – | (363) | (1,132) | (706) | (990) | (957) | ||||||||

| – | 674 | 2,103 | 1,311 | 1,839 | 1,778 | ||||||||

| – | 67% | 67% | 67% | 67% | 67% | ||||||||

| – | 310 | 2,677 | 1,518 | 2,245 | 2,025 | ||||||||

| – | 207 | 1,785 | 1,012 | 1,497 | 1,351 | ||||||||

| 0% | 326% | 118% | 129% | 123% | 132% |

ANSWER

|

Discounted Cash Flow Analysis: |

||||||||||

|

Net Income |

3,471 |

3,877 |

23,074 |

27,581 |

32,830 |

39,005 |

46,264 |

54,793 |

64,807 |

76,562 |

|

Depreciation |

7,650 |

8,530 |

9,393 |

10,409 |

11,534 |

12,781 |

14,162 |

15,693 |

17,390 |

19,269 |

|

Increase in CA |

-5,098 |

-5,074 |

-12,413 |

-10,402 |

-12,118 |

-14,117 |

-16,447 |

-19,160 |

-22,322 |

-26,005 |

|

Increase in CL |

6,310 |

6,053 |

7,405 |

4,349 |

4,844 |

5,401 |

6,027 |

6,733 |

7,528 |

8,425 |

|

LT Invest |

-8,800 |

-8,633 |

-10,154 |

-11,252 |

-12,468 |

-13,816 |

-15,309 |

-16,964 |

-18,798 |

-20,830 |

|

ATICF |

1564 |

1741 |

2036 |

2074 |

2103 |

2118 |

2118 |

2096 |

2049 |

1968 |

|

Free Cash Flow |

5,098 |

6,493 |

19,342 |

22,760 |

26,726 |

31,372 |

36,816 |

43,191 |

50,654 |

59,390 |

|

TV |

742372 |

|||||||||

|

Present Values |

4593 |

5270 |

14143 |

14993 |

15860 |

16773 |

17733 |

18742 |

19802 |

20916 |

|

Present Value of TV |

261452 |

|||||||||

|

NPV |

410276 |

|||||||||

The table above shows the NPV analysis of the company. The detailed proforma statements are present in the attached excel. Based only on the NPV analysis the investment will be a good opportunity for the company as the net present value of the complete company is more than the worth of the company that it will achieve 10 years from today in terms of its net value on the balance sheets.

Most of the growth factors have been taken as the average of the units in East Germany and West Germany. As the part of the company has already reached its maturity state and is growing at the perpetual growth rate where it has saturated, the same has been used as the perpetual growth rate of the complete company (at 3%).

To account for the WACC the cost of debt (interest rate) has been used as the cost of capital as most of the funding will be coming from raising debt itself. However, we do not use the after-tax cost of debt and use the pre-tax cost of debt to account for any changes and a worst-case scenario that is possible. The same also accounts for the 75% dividend pay-out policy which is a much bigger cost of capital. A complete account of the same will not leave room for development for the company and the evaluation by taking 75% of dividend pay-out ratio completely into account will be unfair in the NPV analysis. Thus, only the pre-tax portion of interest rate has been used as the WACC.

The NPV analysis shows that the project is a safe investment and should yield profits for the company in the foreseeable future. However, the NPV of the project is not the risk that the company faces. The risk is rather more operational. The risk that the company faces is the increase of its operations in a new market. The company has definitely worked in that area but that was in a pre-war era and years ago. The market conditions have changed and that has not been accounted for in the analysis at all. The default rate on the accounts receivable in a new working territory is too low and that might lead to unforeseen losses. The same is applicable to the very high working capital cycle which might cause liquidity issues to the company. The risk of working in an unknown market is the biggest one which the board of the company should recognise soon and work to control the same.

Among all the risks that the company faces Max is the key to mitigating the issues and thus his compensation should be high enough to reward his efforts which will bring increased revenues to the company. However, at the same time the compensation plan should also motivate him to continuously strive for increasing the performance of the business which a flat compensation plan will not be able to do. There is a need to increase his basic compensation and a 10% increase in his basic pay should be rational taking into account the 11% cost of capital for the company. His bonuses should be split into a tiered structure. Currently the sales are projected to grow by 30% in the upcoming years in the new markets. Thus, a mere achievement of the projections should not be a cause of increased rewards for any employee. The commission till 30% should remain the same at 0.5%. There should be an increase in the commission post that. For any increase in sales post 30% per year the commission should be 0.8%. Similarly he should have further bonuses like product penetration into new segments and if he is able to help with the distribution system then commissions based on the decrease in working capital cycle of the company.

The current dividend policy of the company aims to increase the dividend pay-out to 75% and hold it stable at that value. The proposal at the onset itself seems slightly more lavish then it should be. The aim of the company should be increasing its growth in the new market during the initial years and not increasing the income of its shareholders at the very onset. Such a high dividend pay-out ratio will leave very less cash in the accounts of the company which can lead to liquidity issues for the management if the new venture falls back. The risk of the new market has simply ben ignored here. The priority here should be to build a strong foundation for the company by setting up wholly owned distribution systems in the new market and move to dividend only after that. Even then the dividend pay-outs should not be as high as they have been proposed currently. A better dividend policy would be to hold on dividends completely for the next 5 years till when the company can utilise the cashflows to consolidate its operation and then have a reasonable ratio around 25-35% which will yield a reasonable income for the investors and at the same time allow the company to utilise its income for further expansion.

Financial Model

| Assumptions: | Perp. Growth | 3% | |||||

| Sales Growth | 17% | Doubtful Accounts/Accounts Receivables | 0.02 | R-WACC | 11% | ||

| COGS/Sales | 67% | Inventory to Sales | 0.14 | ||||

| Depreciation | 10% | Increase in Gross Property Plant | 11% | ||||

| Interest Rate | 11% | Other Current Liabilities/Sales | 0.11 | ||||

| Csh/Sales | 12% | Payables to Sales | 0.05 | ||||

| Tax Rate | 35% | Dividend Payout | 75% | ||||

| Days of Sales | 65.5 |

| YEAR | |||||||||||

| 1992 | 1993 | 1994 | 1995 | 1996 | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 | |

| Income Statement: | |||||||||||

| Sales | 102,356 | 113,355 | 124,147 | 144,632 | 168,496 | 196,298 | 228,687 | 266,420 | 310,379 | 361,592 | 421,254 |

| CGS | (88,411) | (97,771) | (106,928) | (96,462) | (112,378) | (130,920) | (152,522) | (177,689) | (207,007) | (241,163) | (280,955) |

| Depre | (7,650) | (7,650) | (8,530) | (9,393) | (10,409) | (11,534) | (12,781) | (14,162) | (15,693) | (17,390) | (19,269) |

| Operating Margin | 6,294 | 7,935 | 8,689 | 38,776 | 45,709 | 53,843 | 63,384 | 74,569 | 87,679 | 103,039 | 121,030 |

| Allowance for Doubtful Accounts | (19) | (188) | (46) | (145) | (86) | (100) | (116) | (135) | (158) | (184) | (214) |

| EBIT | 6,275 | 7,747 | 8,643 | 38,632 | 45,623 | 53,743 | 63,267 | 74,434 | 87,521 | 102,855 | 120,816 |

| Interest | (2,085) | (2,406) | (2,679) | (3,133) | (3,191) | (3,235) | (3,259) | (3,258) | (3,225) | (3,152) | (3,028) |

| EBT | 4,190 | 5,341 | 5,964 | 35,499 | 42,432 | 50,508 | 60,008 | 71,176 | 84,296 | 99,703 | 117,787 |

| Taxes | (1,467) | (1,869) | (2,087) | (12,425) | (14,851) | (17,678) | (21,003) | (24,912) | (29,504) | (34,896) | (41,226) |

| Net Income | 2,724 | 3,471 | 3,877 | 23,074 | 27,581 | 32,830 | 39,005 | 46,264 | 54,793 | 64,807 | 76,562 |

| Dividends | (2,043) | (2,604) | (2,908) | (17,306) | (20,686) | (24,623) | (29,254) | (34,698) | (41,094) | (48,605) | (57,421) |

| Retained Earnings | 681 | 868 | 969 | 5,769 | 6,895 | 8,208 | 9,751 | 11,566 | 13,698 | 16,202 | 19,140 |

| Balance Sheet | |||||||||||

| Cash | 12,283 | 13,603 | 14,898 | 17356 | 20219 | 23556 | 27442 | 31970 | 37246 | 43391 | 50551 |

| Accounts Receivable | 13,982 | 16,408 | 18,723 | 25954 | 30237 | 35226 | 41038 | 47810 | 55698 | 64888 | 75595 |

| Allowance for Doubtful Accounts | (140) | (328) | (374) | (519) | (605) | (705) | (821) | (956) | (1,114) | (1,298) | (1,512) |

| Inventories | 14,330 | 15,870 | 17,381 | 20248 | 23589 | 27482 | 32016 | 37299 | 43453 | 50623 | 58976 |

| Total Current Assets | 40,454 | 45,552 | 50,627 | 63,040 | 73,441 | 85,559 | 99,676 | 116,123 | 135,283 | 157,605 | 183,609 |

| Investments & Other Assets | 3,914 | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 |

| Gross Property Plant & Equipt. | 76,500 | 85,300 | 93,933 | 104,087 | 115,339 | 127,807 | 141,622 | 156,931 | 173,896 | 192,693 | 213,523 |

| Accumulated Depreciation | (49,961) | (57,611) | (66,141) | (75,534) | (85,943) | (97,477) | (110,257) | (124,419) | (140,113) | (157,502) | (176,772) |

| Net Property Plant & Equipt. | 26,539 | 27,689 | 27,792 | 28,553 | 29,396 | 30,330 | 31,365 | 32,512 | 33,783 | 35,191 | 36,752 |

| Total Assets | 70,908 | 76,242 | 81,419 | 94,593 | 105,837 | 118,889 | 134,041 | 151,635 | 172,066 | 195,796 | 223,361 |

| Bank Borrowings (Short Term) | 7,891 | 12,651 | 16,977 | 21,105 | 21,636 | 22,032 | 22,251 | 22,241 | 21,940 | 21,274 | 20,153 |

| Accounts Payable | 5,328 | 5,668 | 6,207 | 7,232 | 8,425 | 9,815 | 11,434 | 13,321 | 15,519 | 18,080 | 21,063 |

| Other Current Liabilities | 11,259 | 12,469 | 13,656 | 15,909 | 18,535 | 21,593 | 25,156 | 29,306 | 34,142 | 39,775 | 46,338 |

| Total Current Liabilities | 24,478 | 30,788 | 36,841 | 44,246 | 48,595 | 53,439 | 58,840 | 64,868 | 71,601 | 79,129 | 87,554 |

| Long Term Debt: Bank Borrowings | 11,066 | 9,222 | 7,378 | 7,378 | 7,378 | 7,378 | 7,378 | 7,378 | 7,378 | 7,378 | 7,378 |

| Shareholders’ Equity | 35,364 | 36,231 | 37,201 | 42,969 | 49,864 | 58,072 | 67,823 | 79,389 | 93,087 | 109,289 | 128,430 |

| Total Liabs. & Stkhldrs’ Eq. | 70,908 | 76,242 | 81,419 | 94,593 | 105,837 | 118,889 | 134,041 | 151,635 | 172,066 | 195,796 | 223,361 |

| Discounted Cash Flow Analysis: | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | |

| Net Income | 3,471 | 3,877 | 23,074 | 27,581 | 32,830 | 39,005 | 46,264 | 54,793 | 64,807 | 76,562 | |

| Depreciation | 7,650 | 8,530 | 9,393 | 10,409 | 11,534 | 12,781 | 14,162 | 15,693 | 17,390 | 19,269 | |

| Increase in CA | (5,098) | (5,074) | (12,413) | (10,402) | (12,118) | (14,117) | (16,447) | (19,160) | (22,322) | (26,005) | |

| Increase in CL | 6,310 | 6,053 | 7,405 | 4,349 | 4,844 | 5,401 | 6,027 | 6,733 | 7,528 | 8,425 | |

| LT Invest | (8,800) | (8,633) | (10,154) | (11,252) | (12,468) | (13,816) | (15,309) | (16,964) | (18,798) | (20,830) | |

| ATICF | 1564 | 1741 | 2036 | 2074 | 2103 | 2118 | 2118 | 2096 | 2049 | 1968 | |

| Free Cash Flow | 5,098 | 6,493 | 19,342 | 22,760 | 26,726 | 31,372 | 36,816 | 43,191 | 50,654 | 59,390 | |

| TV | 742372 | ||||||||||

| Present Values | 4593 | 5270 | 14143 | 14993 | 15860 | 16773 | 17733 | 18742 | 19802 | 20916 | |

| Present Value of TV | 261452 | ||||||||||

| NPV | 410276 | ||||||||||

Looking for best Finance Assignment Help. Whatsapp us at +16469488918 or chat with our chat representative showing on lower right corner or order from here. You can also take help from our Live Assignment helper for any exam or live assignment related assistance.