QUESTION

Topic:-ANALYSIS OF THE IMPACT OF VAT IMPLEMENTATION ON CONSUMER PURCHASING BEHAVIOR IN BAHRAIN

GUIDELINES

1. Clear project title (addressing some business problem; the title should be able to capture the “gap” or “problem” to a good extent) 200 words

2. Project rationale: A clear statement of the research issue under investigation, specifying the research question or questions you want to answer. The idea is, at every stage of the project, always ask yourself: why are you doing what you are doing? Have you read some literature and identified a gap? Or, do you have experience and you know about some existing problem, which you will try to resolve/address through your work? It is important to have the focus of the research clear – in this sense, you need to justify (a) why you chose the topic you did, (b) why you chose to conduct the research in the setting/ organisation chosen; and (c) what need/gap you will meet/close. Will you be able to provide some implications/ recommendations for practice? Usually, a business research project is expected to do that.

300 Words

3. Background and Literature review: Write few paragraphs introducing the industry/market/company/etc. and about some existing literature on the topic. This usually helps you in identifying the gap. And the gap is what you are trying to address. Later on, you will be able to expand this part in greater detail. But for now, 2-3 paragraphs would be sufficient to briefly outline the current state of knowledge on the topic chosen. You should aim to include about 10 key academic references for now. Please make sure to clearly indicate the conceptual framework and associated hypotheses, if applicable. 1000 words

4. Methodology: Write a paragraph briefly explaining what your methodological approach is – refer to the “research onion” by Saunders et al. so as to make sure you include all the details that should be discussed in this chapter. Also, what is the population and what is your sample size (also, what is your sampling method and sampling technique)? What is your data collection procedure and instrument (and how was it or will it be developed)? Are you considering using interviews or survey questionnaires or observation or something else? Do you have access, for example, to documents and archives? Furthermore, what is the data analysis method that you intend to use? Do you estimate limitations or constraints you may encounter along the way (for example, time constraints, budget constraints, ethical constraints, etc.?). etc. etc. 600 words

5. Expected outcome: Write a brief paragraph about what you think we may learn from reading your final work. Will you be able to draw some implications for practice? Some specific and practical advice for managers? Advance knowledge on the topic? Or anything else you may think of at this stage. To whom would your work be useful? 300 words

6. Project timetable: It may be useful to provide an outline of the project timetable, noting the key stages in the project, for example: 100 words

a. Start date of the project and estimated completion date

b. Period of literature review (2 months? 3 months? etc. etc.)

c. Period of Data collection (1 month, 2 months?)

d. Period of Data transcription (2 weeks? One month?)

e. Period of Data analysis and write-up (3 or 4 months? 5 months?)

f. Recommendations (1 month, 2 months?)

g. Conclusions

Think of how much time you have overall and try to allocate accordingly to each of the stages you envisage.

NOTE: You may not have an answer to all of these questions for now, but try to write few paragraphs including as much information as possible with regards to the issues I raised above. Couple of pages are more than sufficient to make a good and clear case, which you can then explore further. Kindly let me know if you have any questions or need further clarifications.

ANSWER

ANALYSIS OF THE IMPACT OF VAT IMPLEMENTATION ON CONSUMER PURCHASING BEHAVIOR IN BAHRAIN

Abstract

This dissertation has involved critical analysis based on impacts of VAT system on consumers’ purchasing behaviours. Chapter 1 has involved critical discussion based on key issues of VAT system in Bahrain. Along with this, research objectives and research questions have been formed. Research rationale and background of concerned research topic have been discussed in depth. This chapter has explained impact of VAT implication on the purchase behaviour and the process of implementing VAT system. It has discussed affects regarding the issues faced by the business organisations of Bahrain.

The chapter 2 has involved critical discussion taking a number of literary sources into consideration. This chapter has been evaluated that positive impacts of VAT and risks associated to implement VAT system.

Then chapter 3 has involved discussions on research methodology. Positivism research philosophy, inductive research approach descriptive research methods have been involved. Both primary and secondary data analysis processes are included. IBM SPSS has been used for analysing survey data which has been conducted by talking 98 employees of Bahrain supermarkets. A non purposive random sampling technique has been followed here.

Then chapter 4 has involved data analysis in which primary quantitative data analysis and thematic data analysis are included. This chapter has set 4 themes based on the objectives set by the researcher.

Chapter 5 of this research study has been concluded that implementation of VAT policies can be highly effective for developing the overall economical growth of the country of Bahrain. Moreover, rapid enhancement of VAT over daily products has a huge negative impact on customers’ purchasing power. On the other hand inflation has a huge effect on the money reduction of customers in their earned money. On the other hand, most of the organisation of Bahrain can affect mostly by implementing the VAT policies. Thus, their overall sales rate has been decreased. Thus, some recommendations have been provided for managing the VAT rate. Though it can be helpful for developing the economic growth, thus, this research project has several future scopes.

ACKNOWLEDGEMENT

It provides me immense pleasure to present my dissertation entitled as “THE IMPACT OF VAT IMPLEMENTATION ON CONSUMER PURCHASING BEHAVIOR IN BAHRAIN”. This topic of research has helped me to gather immense knowledge about how VAT system can be effective to control consumers’ purchasing behaviours.

I wish to extend most sincere gratitude for those who have helped me to lead this research work towards a reality. Firstly, I thank those who have helped me to gather data throughout the research. I would like to like to present heartiest thanks towards my professors who have helped me to understand this topic and have also helped me to land into a conclusion in this study. I would also like to thank my fellow mates as well as friends who provided me with enough assistance to reach a definite goal. I acknowledge support of batch mates, supervisors as well as professors for this study and I declare to be solely responsible for shortcomings of this research.

Table of Contents

Chapter 1: Introduction

1.1 Introduction

1.2 Problem Statement

1.3 Background of research

1.4 Research aim

1.5 Research objectives

1.6 Research questions

1.7 Rationale of the research

1.8 Significance of research

1.9 Dissertation structure

1.10 Summary

Chapter 2: Literature Review

2.1 Introduction

2.2 Concept of VAT AND GOVT REGULATIONS

2.3 Risk associated with VAT implication

2.4 Consumers’ satisfaction and consumption habit

2.5 Positive aspect of VAT

2.6 Influence of VAT increase on consumer prices

2.7 Price-elasticity of consumers

2.8 Theory and model

2.9 Conceptual framework

2.10 Gap in literature

2.11 Summary

Chapter 3: Research methodology

3.1 Introduction

3.2 Research outline

3.3 Research philosophy

3.4 Research approach

3.5 Research design

3.6 Research method

3.7 Data collection method

3.8 Data analysis

3.9 Validity and reliability

3.10 Ethical consideration

3.6 Limitations of research design

3.12 Summary

Chapter 4: Data analysis

4.1 Introduction

4.2 Data analysis

4.3 Summary

Chapter 5: Conclusion

5.1 Conclusion

5.2 Linking with objectives

Objective 1

Objective 2

Objectives 3

Objective 4

5.3 Recommendations

5.4 Limitations

5.5 Future scope of research

Reference list

Appendices 84

Appendix 1

List of tables

Table 3.1: Research outline

Table 4.1: Number of Gender participants

Table 4.2: Age Groups of Participants

Table 4.3: Working experiences of the participants

Table 4.4: Statistic Data on survey questions 3 to 5

Table 4.5: Statistic Data on survey questions 6 to 10

Table 4.6: Responses about customer purchasing intention

Table 4.7: Responses regarding customer buying behavior

Table 4.8: Response to customer dissatisfaction about VAT application

Table 4.9: Responses regarding supermarket loss

Table 4.10: Responses about the imposition of VAT impacted customer arriving at the supermarket

Table 4.11: Response to VAT increases impact sales margin of supermarket

Table 4.12: Responses about the law of Bahrain impacting country economy

Table 4.13: Responses about the law of Bahrain for the betterment of mankind in Bahraini

List of figures

Figure 1.1: The price change in January, 2018

Figure 1.2: The price change in February-November, 2018

Figure 1.3: Dissertation structure

Figure 2.1: Price elasticity and demand theory

Figure 2.2: Bertrand model

Figure 2.3: Cournot theory

Figure 2.4: Conceptual Framework

Figure 3.1: Types of research philosophy

Figure 3.2: Types of research approach

Figure 3.3: Types of research designs

Figure 3.4: Types of research methods

Figure 3.5: Data collection method

Figure 3.6: Methods of data analysis

Figure 4.1: Total Number of gender participants

Figure 4.2: Participants age group

Figure 4.3: Participants working experience

Figure 4.4: Responses for customer purchasing intentions

Figure 4.5: Responses for customer attitude for purchasing a product

Figure 4.6: Responses to the dissatisfaction of Customers about VAT implementation

Figure 4.7: Responses about supermarket loss

Figure 4.8: Responses about the imposition of VAT impacted customer arriving at the supermarket

Figure 4.9: Response to VAT increases impact sales margin of supermarket

Figure 4.10: Responses about the law of Bahrain impacting country economy

Figure 4.11: Responses about law of Bahrain for the betterment of mankind in Bahraini

Chapter 1: Introduction

1.1 Introduction

Value added tax (VAT) is a type of indirect consumption tax which possesses multiple stages. VAT is a fixed and standard percentage of tax charges, imposed on every product and service additionally on the marked price which the customers are bound to pay. This tax charges are only dependent on the price value of the goods and services and do not change with product range and variety. Moreover VAT possesses a profound influence on the customers purchase capacity. As due to additional VAT charges the price gets higher and the consumers need to pay the marked price of the goods and the additional VAT charges on it. Bahrain, a small island country in the Persian gulf of Saudi Arabia, has brought a revolutionary change in their economy by introducing VAT. Bahrain incorporated this VAT system along with other Gulf countries in the year 2017. However, the official implementation of VAT system in Bahrain was from 1st January, 2018. Initially a 5% VAT charges has been imposed on the products and services in Bahrain. This current research focuses on the newly implemented VAT services in Bahrain and its effect on the customer purchasing behaviour. The consumer purchasing behaviour tendencies are analysed in the context of VAT implementation and price hike. The concept of VAT, government regulations, consumption habit of the customers, and price elasticity of the customers are evaluated in a thorough manner along with the relevant theories and models.

1.2 Problem Statement

Across the entire world, significant attention is given of the VAT reforms and structure. According to Munteanu et al.(2016, p.108), the VAT taxation system owns a significant contribution on the government revenue, economic development and growth. As this VAT charges increasers the expenditure of consumption in an effective manner, it possesses a significant influence on the purchase behavioural pattern of the consumers. Setiawan (2018, p.5) suggested that, the implementation of VAT changes the price range and consumption behaviour of customers as well. After implementation of VAT system in Bahrain, the business sectors of Bahrain are facing a reduction in the customers purchase rate. The companies have reported a dramatic change in their sales in the last few years. The additional charges of VAT are considered to influence the customer’s purchasing tendency, which is a matter of concern in an obvious manner. This research is focused to analyse these effects of VAT on the purchasing behaviour of the customers of Bahrain.

1.3 Background of research

VAT is considered to be the most essential method of collecting tax by the government in order to initiate development and growth in a specific country. Haibara (2017, p.632) opined that, the indirect way collecting consumption tax collection is a type of governmental strategies for collecting funds for welfare process. This has been analysed that government ensures the fact that imposed amount of tax is appropriate for the business operations to function at normal scale without getting hampered by changes.

The Gulf region of Saudi Arabia including Bahrain has been considered to be an attractive as well a slow tax environment. Hence, in order to keep pace with the changing economic situation, and to be a part of developmental reforms, Gulf Cooperation Council has signed an agreement for introducing the system of value added tax on the goods and services available at the rate of 5% in the year 2018 (Home.kpmg, 2019).

The implementation of this VAT system have several influences on the business, taxpayers, and the purchasing behaviour of consumers both indirect and indirect manner. The agreement of VAT signed by the cooperation council of Arab has developed a framework on the basis of which the system of VAT can be implemented in an effective manner. Whitehouse and Nurmi (2016, p.78) stated that, the amount of VAT is calculated on the basis of the total consumption of goods and services by the consumers. However the businesses have the provision to claim the credit for the paid VAT on their business oriented expenditures. [Refer to Appendix 1]

Hence the VAT has the impact on each and every business which is related with the field of supplying products and services. Saudi Arabia’s consumer price inflation has increased to 3% after introducing the 5% VAT system (Andrew Torchia, 2019). A bulk of changes caused by the system of VAT was prominently visible in the monthly price hike since the month of January, 2018. The consumer price index shortly known as CPI increase is 3.9% m/m in the Saudi Arabia and 2.7% m/m in the UAE (Andrew Torchia, 2019). The main reason behind this hike in inflation in Saudi is the prominent cut in the fuel subsidies which has also been implemented along with the VAT and caused a rise in the transport cost by 12.7% m/m (Andrew Torchia, 2019).

Additionally in the initial month of January, 2018 there was a prominent effect in the hospitality, food, and recreation, communication and healthcare division as well (Nbr.gov.bh, 2019). The education cost has decreased by 1% in a positive manner in UAE. The non oil priVATe sectors have grown by 1.7% in the last year (Nbr.gov.bh, 2019).

Figure 1.1: The price change in January, 2018

(Source: Nbr.gov.bh, 2019)

Afterwards gradually some positive effects also came out in several fields. The communication price, food prices, transport and hospitality price decreased in a gradual manner (Nbr.gov.bh, 2019).

Figure 1.2: The price change in February-November, 2018

(Source: Nbr.gov.bh, 2019)

The price changes and the additional charges on the marked price are assumed to be the main factors which are affecting the purchasing behaviour of the consumers.

1.4 Research aim

This research aims to analyse the effects of VAT implementation on the purchasing behaviour of the customers in the country Bahrain. This research study has the target to identify the major impacts of VAT on the national economy as well as the price change issue.

1.5 Research objectives

There are several major objectives of this research which are related to the impacts of VAT on the purchasing capacity of the consumers. The main objectives are as follows,

-

To assess the impacts of VAT implication on the purchase behaviour of consumers in Bahrain.

-

To identify how implementation of VAT system is affecting the sales rate of business organisations.

-

To identify the issues faced by the business organisations of Bahrain after the VAT implementation.

-

To analyse the positive aspects of VAT from the perspective of the nation and its people.

-

To identify the steps which can mitigate the negative impacts of VAT system in Bahrain?

1.6 Research questions

-

What is the influence of VAT implementation on the purchase capacity of the customers in Bahrain?

-

How VAT implication is affecting the sales rate of several companies responsible for manufacturing goods and services?

-

What are the issues faced by the business companies of Bahrain after implementing the system of VAT?

-

How this system of VAT is beneficial for the nation and its people?

-

What steps can be incorporated to minimise the negative effects of VAT implementation in Bahrain?

1.7 Rationale of the research

The main issue on which this research is shedding light upon is the fact that the VAT implication has a great influence on the purchasing behaviour of consumers in Bahrain. On 1st january, 2018 the government of Bahrain has implemented a system of VAT. The VAT charge was set to 5% extra on the price of the products and services. This has greatly influenced the price range along with the customers purchasing pattern and behaviour.

This VAT implication in Bahrain is considered to be a major issue as this has introduced an additional charges of 5% on the marked price of the goods and services which has to be paid by the consumers in a compulsory manner (Nbr.gov.bh, 2019). After implementation of this VAT system, several business organisations have reported a dramatic change in their sales rate within a few months (Andrew Torchia, 2019). The VAT system is basically adding up some extra tax charges on the products which are considered to be one of the major reasons behind a sudden hike in the price range of goods and services. This price hike can dominate the purchasing tendencies of the customers in a significant way.

The country Bahrain of Saudi Arab has implemented the VAT system in a practical manner from 1st january, 2018 (Nbr.gov.bh, 2019). After this implementation of VAT system, several changes in the price in the field of hospitality, food, and recreation, communication, and healthcare division has been observed in the last one year (Andrew Torchia, 2019). Hence this is assumed that this price changes has the capability to influence the purchasing behaviour of the customers.

This research is focused to address the impacts of VAT implementation on the purchasing patterns of the consumers in Bahrain. The concept of VAT, the government rules and policies to implement it, the associated risk factors, consumption habits of customers, price elasticity of consumers are the aspects which are analysed in this research to fulfil the demand of the issue.

1.8 Significance of research

This current research is focused on the impacts of VAT implementation in Bahrain on the purchasing tendencies of consumers. This research issue is considered to be significant and unique as well. The implication of VAT has a great influence on the national economy of Bahrain and this research can be effective to provide an adequate resource. The VAT system has been introduced in Bahrain in the month of January in 2018 (Nbr.gov.bh, 2019). This additional tax charges has affected the purchasing capacity of the customers as they have not get habituated with this price hike due to VAT charges. That is why the business market and the sales rate of products are going through a huge loss after implementation of VAT policies. This research is considered to be significant to identify the factors responsible for this unstable condition at Bahrain. This research paper is also going to highlight the positive aspects of VAT system as well. The addressed issues and challenges in this report will be effective to identify an alternative to deal with this implication of VAT system.

1.9 Dissertation structure

Introduction

Literature review

Research methodology

Analysis and discussion

Conclusion and recommendation

Figure 1.3: Dissertation structure

1.10 Summary

The above chapter is all about introducing the issue that the VAT implementation has a major impact on the purchasing behaviour of consumers in Bahrain. This chapter has highlighted that facts and data in this context of VAT implementation in Bahrain. The associated issues related to this VAT implementation such as, price change, drop in the sales rate and more. The context of this research is mentioned along with the significance of it. The background and context in which vthe system of VAT was implemented in Bahrain, the responsible committee for this implementation, the immediate effect of VAT implementation in the business market all are mentioned above.

Chapter 2: Literature Review

2.1 Introduction

This chapter is aiming to discuss the concept of Value Added Tax (VAT) with its background as well as its impact on the economy of a country. This study is also going to evaluate the impact of VAT on the purchasing power of Customers. It is going to discuss the regulations done by the Government of Bahrain as well as risks associated with the imposition of VAT. Here, the satisfaction of the consumer and the consumption habit with the positive impact of VAT is going to discuss. Influence of VAT increase on prices of the consumer as well as Price-elasticity of consumers is going to analyze. This chapter is also going to evaluate the possible market scenario of Bahrain with the help of theories. Lastly, it is also going to evaluate the literature gap regarding this topic.

2.2 Concept of VAT AND GOVT REGULATIONS

Value Added Tax is one of the most important collection processes of tax which is performed by the Government of any country. This process is generally done with the aim to develop a specific country. As per the views of Benzarti et al. (2017, p. 1), Value Added Tax has the capability to affect a large part of the economy of the whole world with all countries that are members of Organization for Economic Co-operation and Development. This method of tax collection is basically a mode of indirect collection and it is a strategy that is taken by the government aiming to arrange funds in order to develop as well as the welfare method. It can be evaluated that a government needs to assure that the imposition is in the accurate amount of tax. It is necessary for business which can be operated in a customary scale and also avoiding much incorporation of changes. The surplus burden of a product that is done on purchase is generally used to impose aiming in social convenience. The VAT has a method of calculation that is done by

VAT= [Price of product + (Tax/100 * Price of product)].

On the other hand, as per stated by Pomeranz (2015, p. 2), Value Added Tax is one of the sharp examples of a tax that is believed has a function in facilitating of enforcing by the structure of in-built incentive. It is generally generated by a party which is basically the third one to report trial on paper for transaction among many firms and this process helps in hiding transaction from the Government of any country. The VAT is not only a quantitative expression but actually an additional amount which is used to charge by the Government on the time of purchasing of any articles. On the contrary, according to Kleven et al. (2016, p. 19), VAT needs all firms to maintain the accounts of their purchase as well as sales and also to pay taxes for their sales of the net of paying. It can be said as every firm has an inducement for sales of under-report as well as purchases of over-report. For this forming an alternative incentive over businesses engaging in the transactions of arm-length is done.

As per the views of Pomeranz (2015, p. 6), Value Added Tax has to pay by people in every stage of production that is firms used to pay the specific tax on the variation among the sales of total and the cost of total input. There is a difference in between VAT and that of Retail tax. This difference is basically the process of collection of tax and the person the used to remit the tax to the government. VAT sometimes used to make a hike of the price of a specific product and in turn, it generally imparts additional pressure on consumers. The business also during this time has a tendency to getting suffered due to loss for the incorporation of VAT on sales of the commodity. Affect of VAT on customers is enormous and requires specific execution for reducing confusion.

As per the views of Bannaga (2017), more than 150 countries have implemented VAT, the admissible policies of VAT as incorporated globally has an influential effect on the commerce styles of above 90% volumes of overseas trade. The government of the country Bahrain has taken inventiveness of incorporate VAT on the purchase of commodity aiming for a collection of taxes. Almost every country that is developing has initiated to incorporate VAT on the product for collection of revenue. This process has been considered as the best strategies taken by the Government for the method of tax collection. This collected tax is utilized by the Government in the procedure of development for the country and this is done by Government. Proper collection of taxes has an important role to play in a country. The taxes help in the enhancement of economical situation of a country with the conventional implication by the practice of Government. The taxes are also used in the development of social conditions as well as development and improvement of infrastructure.

Contradictory, as stated by Terfa et al. (2017, p. 1), one of the most fortuitous improvement incontrovertibly is the VAT that was started on the last half-century with the policy of taxation. No other form of taxes, neither the income tax, have created an effect so rapidly and speedily to such magnitude that the VAT presently existing in more than 150 countries all over the world, comprising Bahrain, Ethiopia also many other countries of Africa. The VAT is one of the fundamental methods by the help of which the government of Bahrain and other countries used to assemble money for the maintenance of their level in the global context. The collected amount of revenue is then utilized in the target for clearance debt as well as to conduct prosperity in the concerned nation. It also has been recognized that 5% of the VAT on every commodity is inculpated by the Bahrain government for the maintenance of equality as well as to bring stability in the nation. Every product with equivalent VAT is appraised to be a fundamental policy incorporated by the Bahrain government. On the other hand, according to Singh (2019, p. 116), VAT has been accepted as a notable contributor to the economical development of any country. The causes and relevance of up surging VAT do not receive any attention virtually, or theoretically and also not in an empirical way. Those developing countries in the gulf require for making a change in their already existing economical structure for introducing growth in their economic condition. However, the low GDP rate of Bahrain has been identified to be an important constraint to the customer’s purchasing power.

2.3 Risk associated with VAT implication

As opined by Alavuotunki et al. (2017, p. 6), VAT has affected in starting a tax system which is more dependent in nature. This dependency is generally on the taxes of flat-rate and in an indirect way and also it has less dependence on escalating direct taxes. By this change has a tendency in reflecting a huge inequality of disposable-income as due to the presence of much less share of direct as well as progressive taxes. Due to the imposition of VAT, business at its initial phases tends to face losses by encountering new policy of tax that is incorporated in of business. But, with the motion of time, the consumers and also sales used to get accustomed to the scenario of business and also initiates its operation with specific alternatives. In the country of Bahrain, the Businesses is basically new to incorporating the VAT and this is the reason why the customers of this country are detecting difficulties for the acceptance of the specific condition of their market.

On the contradictory note, Ots et al. (2016, p. 172) mentioned that changes, whether it will be a positive or, maybe a negative in the VAT, has the potential in creating a dramatic effect on numerous commodity titles on especially the markets of media. There are also other forms of constructions in tax like directed tax credits. These tax forms also have a more affectivity to make stimulate nature in more divergent manufacturing of journalism. The specific realization of the aspect that VAT is basically is an indirect mode that has a function to help themselves, and also for the development of society. It is needed for customers in the country of Bahrain to make acceptance of the hiked prices. However, as per the views of Freund and Gagnon (2017, p. 3), the time when the amount of a VAT is get hiked, in a parallel way domestic prices also used to get increased almost one after one. And, after this incident, the general result is that exporters, as well as importers, used to persist indifferent among the markets of domestic as well as foreign. This is basically due to the hiking in the tax is counterbalanced by the elevation in the price of domestic. Enforcement of VAT in the economy of the country Bahrain has a result in making increased in the instability of business. The unexpected increase in liability of businesses also has contrived the easy execution of the operation of a business in the markets of Bahrain.

2.4 Consumers’ satisfaction and consumption habit

Customer satisfaction is considered to affect several aspects of the company such as, sales rate, growth, revenue, expenses, net income and more. The term customer’s behaviour refers to recognising the customer needs their demand, preference and financial purchasing plan which can be afforded. Viard (2018, p.405) stated that, the price of products and services can play a significant role in influencing the purchasing power of the customers. Along with the increase in the price range people may reduce the rate of purchasing it. On the other hand if the price gets down the people increase the rate of buying it.

Similarly, Vegh and Vuletin (2015, p.342) opined that, if the price gets increased, the customer will show a tendency to buy an alternative product with a lower price range. In case of similar products and services the customers often go for the cheaper one as the price rises. Sulaiman et al. (2018, p.465) stated that, wrong tax at the wrong situation may put people or consumers in high pressure. In this same context Lee and Fay (2017, p.132) stated that, increased price because of VAT implementation may distort the consumption habit of the customer base in a huge manner. As per Firsova et al.(2018, p.238), commonly there are four major areas which can influence the purchase behaviour of the customers such as the social, personal, cultural and psychological. According to Viard (2018, p.405), the cultural factor itself includes the social aspects which are dependent on the income, wealth, occupation, status and personal attributes. On all these personal factors, age used to play a major role. Along with the change in age factor, the opinion and concept of consumption gets changed. The most essential factor considered here is the economic condition and capacity. The purchase behaviour of the customer gets hugely influenced by the affordability. The social status also impacts upon the purchase pattern as the purchase capacity and style is completely different between the high class and low class people. The psychological factors of people such as choice, demand, outlook matters a lot in influencing the purchase habits of the consumers. The choice and outlook matters here, because the person’s purchase pattern gets generated from there only.

2.5 Positive aspect of VAT

VAT system has been implemented by several countries across the world and is possessing a tremendous positive influence on the national economy of that country. In order to introduce overall development in a country, the essential factor is to bring positive changes in the economic dynamics. VAT implication is considered to be effective in order to enhance the economic status of the country. Terfa et al. (2017, 87) stated that, the implementation of equal tax charge is considered to be highly beneficial for maintaining proper administration. Ching et al. (2017, p.460) suggested that, an equal distribution of tax charges just on the basis of price range is considered to initiate trust and procedural justice factor in an effective manner. This makes the government able to conduct administration activities in a proper manner and take up measures for the benefit of the country. Several developmental approaches such as educational status, health facilities of Bahrain along with lifting up the people above the poverty line can be made possible with an appropriate implication of VAT system. Additionally Andoh et al.(2019, p.152) stated that, in comparison to other tax charges the tax evasion probability is minimum in value added tax. Hence this taxation system can reduce the tax gap in an effective manner and enhance the national economic condition. A fixed taxation plan helps a lot to run the supply and demand chain in an effective manner. The VAT tax rate is equal for all companies and organisation and there is no scale of division. Hence in compare to other taxation system this system is easy and smooth to follow.

2.6 Influence of VAT increase on consumer prices

The customer used to suffer the maximum in case of implicating the changes by introducing new government policies related to tax. Artés et al.(2019, p.13) stated that, the main source of tax collection is majorly the local people. The inclusion of 5% excess tax burden through the implication of VAT system on products and services affects the customer base in a huge manner.

The deteriorating purchasing behaviour of the customers after the implication of VAT system by the CCG government affects the business market growth of Bahrain. According to Abaidoo (2016, p.382), in response to this, the customers who are rational by nature will show the tendency to invest their resources in the most appropriate manner. In support to this, Sulaiman et al. (2017, p.469) opined that, the customers invest their money on the necessary commodities only in specific situation of price hike. The decrease in the purchase capacity of the consumers of Bahrain has witnessed a huge loss in the business market operating.

Standard imposition of 5% tax charge on every commodity has been considered to be an irrational output of VAT. Ufier (2017, p.1152) stated that, the Bahrain government has implicated VAT along with the association of six Gulf countries of Saudi Arab. The economic status of all Gulf countries are not the same and that is why the introduction of VAT in the same proportion on every product available in the market of these six concern countries is not justified and appropriate.

2.7 Price-elasticity of consumers

The impact of VAT system on the price change is dependent on the elasticity of two factors such as demand and supply. According to Whitehouse and Nurmi (2016, p.78), the behaviour of customers has a direct relation with the change in the VAT rate. This price elasticity factor usually depends on two factors such as, the substitution effect and the income effect.

When the price of a good rises the alternative option becomes more in demand. As the substitute have a lower price the people shows the tendency to buy it. Terfa et al.(2017, p.92) stated that, in case of VAT theory, as the total effect, income effect and substitution effect rises, the price elasticity also rises accordingly. Every consumer product is governed by the concept of supply and demand. Hence every consumer good is capable to demonstrate the price elasticity factor. Vegh and Vuletin (2015, p.332) stated that, there are various determinant factor\s which influence this price elasticity of demand. Consumers possess a tendency to switch product as the price increases. The elasticity is much more in the more expensive range of products as the customers gets sensitive and affectionate and ready to invest a huge bulk of money for that product or service. Hence the price elasticity of the consumers is considered to be a significant factor which can maintain the sales rate even after the price hike issue.

According to Terfa et al.(2017, p.97), the brand name and the marketing strategy has a huge impact on the price elasticity of demand. The price hike for the well known company products possess less impact on customers in compare to other less known as well as less trusted companies.

2.8 Theory and model

2.8.1 Price elasticity and demand theory

Prices in the market are generally used to be in a dynamic in nature when there is an imposition of various taxes. A similar situation has been noticed when there is an imposition of Value Added Tax which is an indirect tax. Generally, the indirect form of tax in which the VAT is included on producers is used to get make hike their value of costs. This used to also lead in a situation where the shift is in an inward movement in the curve of supply.

After the imposition of the tax, suppliers can choose on the tax for the purpose of passing to consumers. This can be done on the market of Bahrain with creating raising the selling price. This usually depends on the collaboration of elasticity in price of demand. As per the views of Paciello et al. (2019, p. 422), the price of any firm used to put an impact on the value of any firm with two channels. At the initial stage, the price usually affects the degree of profits per consumer as per the standard model of pricing in a firm. On another hand, the price used to put an impact on the dynamic nature of the base of customers. In this context, it generally has an influential effect on the mass of consumers those buying from a firm in the present time from those in future. Elasticity in price also represents whether the firms can be able to pass costs in higher that they used to sustain on to consumers.

Figure 2.1: Price elasticity and demand theory

(Source: Paciello et al. 2019, p. 423)

2.8.2 Bertrand model

According to Albert and Kliemt (2017, p. 7), If there is the lowest price fixed by any business is p, then every firm that is setting the price p are assigned the share identical of demand and all other business sell zero. Profits that are collected will be maximal, in the case, if every firm settles the price which is equal with the monopoly price p max > c.

Figure 2.2: Bertrand model

(Source: Albert and Kliemt 2017, p. 8)

2.8.3 Cournot model

As per the views of Askar et al. (2016, p. 13), the Cournot model is studied by the function of cost which is uncertain quadratic. A haphazard quadratic cost function is incorporated in this model. Every firm that is present in the model has a target in maximizing its profit which is expected as well as it also has an aim in minimizing its undetermined state with making the cost-minimizing. For handling this issue of multi-objective expansion, the expectation, as well as approaches of worst-case, is utilized.

The Cournot model of oligopoly has the character in assuming the firms which are in the rival list and used to manufacture a product which is homogenous in nature. It also in every attempt tends in making maximizing the profits by making choice of the quantity need to produce. In this context, this model can be utilized for the market of Bahrain by identifying the rivalries and setting the pricing in a way that can bring profits. This model will help the market in recognizing that price maybe not equal in costs that are present in most marginal cases. The level of magnitude up to which price of every firm surpasses the marginal cost is basically proportional in a direct pattern. This pattern is with the share of the market of firm and also it is proportional in a inverse way to the demand of market which is elastic in nature.

Figure 2.3: Cournot theory

(Source: Askar et al. 2016, p. 14)

Factors influencing the purchasing power of consumers

The purchasing power of consumers is a term in economics is stated as the number of goods as well as services. These can be bought with the provided sum of currency. There are various factors that influence on the purchasing power of customers. Firstly, price is a major factor playing regarding this as the value of goods as well as services are in the most necessary determinants for this. When there is a rise in the level of price, there is a state of decrease in the power of purchasing is seen. And, at the time when the level of price used to get fall, there is an increase in the power of purchasing. This can be seen if there is a state of equality for other factors.

Real income is another factor that plays the role of the determinant of consumer’s purchasing power. Generally, on the real income of an individual, the purchasing power used to depend. The real income of a person is the quality of money that help in making an adjustment for the time of changes in the prices. Generally, if the real income of an individual used to get increase then that person will be more able to buy more goods and services. The third factor that determines the purchasing power of people is the rate of tax and it is one of the most important factors in this field. In the condition where there is a high rate of tax present, then automatically, the purchasing power of people has a tendency to get decreased as taxes used to lower the real income of people.

The indirect tax also has the tendency to make a rise in consumer prices. Value Added Tax is indirect of tax and also it used to affect the purchasing power of consumers. The imposition of VAT has a great impact on the buying power of consumers. If the rate of VAT imposed is in a less amount and on the luxury product then the purchasing power of the low-income consumers usually does not have much effect. But, if the rate of the imposition of VAT on daily needed products is imposed then it will be going to suffer maximum consumer’s purchasing power. The exchange rate is a factor that used to influence on the purchasing power of consumers. This factor has mainly influences the currency present in a foreign country.

Inflation is another factor that has a serious impact on the purchasing power of consumers. It is the state of a country where too many currencies used to run before too few goods. It generally used to increase consumer prices and automatically make decrease the purchasing power of the consumers in a country. In this situation, the basic goods get an increase in price and these items demand too much amount of currencies get purchased. Inflation also has an impact on the reduction of the money of consumers in the earned money from their saving money. In this situation, the income of consumers used to get increased at the similar rate of inflation. Hence, this similar nature of increase has an adverse effect on the purchasing power of consumers in a country. This situation usually has tendencies in creating a situation of passive income through different businesses or investment in the economy.

2.9 Conceptual framework

VAT implementation

Purchasing power of consumers

Government regulation

Risk associated with VAT

Negative and positive impact on purchasing power

Price elasticity of demand theory

Bertrand and

Cournot model

Marginal cost, competitive price, collusive equilibrium, counot equilibrium, competitive equilibrium

Reduced purchasing power

Figure 2.4: Conceptual Framework

2.10 Gap in literature

In the previous researches on the topic of the impact of VAT implementation on the purchasing behaviour of consumers, many information and literature have been found. The information which was found in previous research has helped to complete this paper. However, there are some literature gap persists regarding this topic in previous studies. Much information relating to this to the topic of VAT implication impact on consumer’s purchasing behaviour. Many theories relating to the purchasing behaviour of consumers have not been clearly found on previous researches. Also, the economy of the different country varies and the effect of direct or indirect taxes also varies on the condition of the economical and other conditions of countries. Hence, these distinct conditions also were not in clearly founded in previous researches regarding this particular topic. In the previous research of the above topic the researcher has failed to observe about the responses of the employees regarding the VAT implementation on the behaviour of the consumer purchase. Thus, in this study, the research will mitigate the previous research mistakes by doing proper survey on the topic by interviewing 98 participants for knowing their opinion regarding the implementation of the VAT. The past mistakes will be rectified in this study by the researcher by doing proper as well as careful research regarding the topic.

2.11 Summary

Different type of taxes either directs or indirect form of tax has variable effect on the economy as well as the purchasing power of the consumers of a country. This chapter has focused on evaluating the impact of VAT on the purchasing power of Customers. It has also discussed the regulations done by the Government of Bahrain as well as risks associated with the imposition of VAT. Here, the satisfaction of the consumer and the consumption habit with the positive impact of VAT has been discussed. Influence of VAT increase on prices of the consumer as well as Price-elasticity of consumers has been analyzed. This chapter has also provided the evaluation of possible market scenario of Bahrain with the help of theories. Lastly, it has evaluated the literature gap regarding this topic. In this chapter, discussion has been completed on the different factors of the VAT which are encouraging the purchasing behaviour of the consumer of the supermarkets. It has also highlighted about the risks of the VAT implementation on the behaviour of the consumers which affecting the supermarkets in a both negative as well as positive manner. It has also focussed on the customer’s needs as well as requirements and satisfaction from purchasing a product from supermarket. This study also reflects about the risk factor of the VAT implementation. It has also states about the positive side about the VAT implementation in this chapter.

Chapter 3: Research methodology

3.1 Introduction

This chapter of the research is focused on developing an overview of the methodologies through which the research has been built-up. Research is a common language which means the exploration of knowledge. This chapter particularly explores all the detailed information about the methodologies in terms of research outline, philosophies, research approaches, designs, data collection method, data analysing tools, ethical considerations and the limitations of research designs.

3.2 Research outline

In this research methodology chapter, includes many methods and strategies are used and the selection of the strategies which is depending on the impact of VAT implementation on consumer behaviour in Bahrain. An Effective research methodology will be used to execute proper research work in a proper organised manner. This research outline conveys the best ideas and tools which are to be taken for the best knowledge acquisition related to this topic.

|

Research Philosophy |

Positivism research philosophy |

|

Research approach |

Inductive research approach |

|

Research design |

Descriptive research design |

|

Data Collection Method |

Primary Data collection |

|

Data analysing technique |

SPSS |

|

Sampling method |

Non-purposive random sampling |

|

Sample size |

Around 150. |

Table 3.1: Research outline

3.3 Research philosophy

This research study has taken positivism philosophy into consideration rather than realism, positivism, and Interpretivism research philosophy. The selection of Positivism is beneficial in conducting proper quantitative study on concerned research topic. As a philosophy, positivism coheres to the view of acquiring the accurate knowledge from the observations. In positivism, the study knowledge is limited from the collective data and it interpreted the objectives. As mentioned by Gabriel (2015, p.335), positivism research philosophy is helpful for researchers to conduct quantitative study based on qualitative discussion. This study has involved this research philosophy which helps the researchers to conduct survey of employees along with analysis theoretical data based on formation of theme.

Figure 3.1: Types of research philosophy

(Source: Influenced by Barquero and Bosch, 2015, p.250)

Besides, positivism philosophy becomes helpful to collect first hand data by forming questionnaire. In case of this research study survey has been conducted by forming 20 survey questions. Thus considering positivism philosophy becomes helpful to gather relevant numeric data based on impacts of VAT implications on consumers’ purchasing behaviours. As the positivism research philosophy is based on collection of factual data, hence realism and interpretivism have been discarded.

According to Singh (2015, p.132), the positive research philosophy is compatible with the perspective of research methodology of knowledge creation as it has increased the conception of the research context. In this research philosophy, the research interpretation of actors has the involvement in organisational flow events with their individual experiences. Positivism has adopted a fair quantitative approach to scrutinize phenomenon, as conflicting with post-positive approach, which aims to explore and recount the depth of phenomenon from a measurable perspective. This research has targeted to introduce the philosophical based research, which has provided the descriptive analysis of positivist philosophy (search.proquest.com, 2019).

3.4 Research approach

In research approaches; there are two different approaches, deductive approach and inductive approach. Between the inductive and deductive approach, the inductive approach has used for the conduction of this research. The Inductive Research approach is normally related with the subjective research and its main target is to generate new theory based on the given data. This approach has used the research questions which are restricting the opportunity of the consumer purchasing behaviour in Bahrain. In words of Murshed and Zhang (2016, p.438), the basic difference between inductive and deductive research approaches focuses on inclusion and exclusion of theoretical aspects in research methods. This concerned research study has emphasized strongly on creating theories and linking statistical data with those theories. Thereby, inductive approach has been taken into consideration while deductive research approach has been discarded.

Figure 3.2: Types of research approach

(Source: Saunders and Bezzina, 2015, p.301)

In case of this research work inductive approach has been taken into consideration for creating a link between research objectives and findings. In this regard, this research approach becomes helpful for researchers to gather necessary theoretical data for having effective and authentic results after linking the statistical findings of survey process with theoretical findings.

According to Alase (2017, p.11), in inductive research methodology, the different types of analytical data approaches is presented that has been used for the data analysis. While using the inductive research approach various possibilities have come forward, but the true possibilities has helped in research to present the result in a modified manner. While using this approach the proper recognition theories used in VAT operating countries and that has done for maintaining the good effective search approach. But this approach affects the research with the limited scope and inaccurate conclusions. According to Daniel (2019, p.51), an inductive research provides the data-informing approach to get the more relevant data. Through the learning analytical data- it has given the research approach to conduct this research.

3.5 Research design

Numerous types of research design are used for the different types of research study. The main aspect of descriptive research design is to elucidate the state affairs as it subsists at present. The study of analysing the impact of VAT implementation on consumer behaviour in Bahrain has used the descriptive research design. The main aspect of descriptive research design is to elucidate the state affairs as it subsists at present. The descriptive design ventures to scrutinise the situations in order to orthodox, what are the standards, that means what can be predicted to happen under the eventual circumstances. According to the views of Kothari and Patel (2015, p.1173), research design is presented as the aggregation of techniques that can be advantageous for researchers to collect relevant data along with analyzing them to have authentic results upon completion of this research work. In case of this concerned study, the descriptive design has been selected whereas the exploratory and explanatory designs have been discarded.

Figure 3.3: Types of research designs

(Source: Influenced by Walliman, 2017, p.11)

Considering this research design can be helpful for researchers to link between existing theories of VAT system and research findings. Thus it appears helpful to have appropriate results based on key changes of consumers’ purchasing behaviours due to implementation of VAT system. Moreover, considering descriptive research becomes helpful to shed light on research problems and use effective data collections techniques to gather most relevant information based on concerned topic.

Besides, it can be stated that descriptive research design appears helpful to use existing theories for understanding research problems. Thus it becomes easier for researchers to deal with statistical findings to have specific results based on changes in VAT system and impacts of Vat system on consumer’s purchasing behaviour in Bahrain. According to Walliman (2017, p.10), the descriptive design depends on the observations as a means of data collection. The observations can take many forms, depending on the sought information types; consumers can have a discussion with and distribution of questionnaires. This research study has taken into consideration of primary quantitative as well as secondary qualitative data. This research has been conducted for detailed analysis of customer’s purchases trends after the implication of VAT. Hence, proper collection of data is beneficial to reaching the proper research problems. Descriptive Research design has helped the study to go in depth of researching the problems of consumer purchasing behaviour in Bahrain.

3.6 Research method

There are two main types of research named as qualitative and quantitative research method. In order to proceed with this research study primary quantitative and secondary qualitative research methods have been taken into consideration. As mentioned by Silverman (2016, p.36), selection of effective research methods are helpful to determine the mode of the research study. In case of this research work, statistical analysis appears essential to understand impacts of VAT system on purchasing behaviour of consumers. Thus, primary quantitative research method has been selected to have statistical data by conducting a survey of 98 employees of concerned organisation in Bahrain. Selection of appropriate research method helps to proceed further in an efficient manner.

Figure 3.4: Types of research methods

(Source: Influenced by Flick, 2015, p.55)

Quantitative research method helps to assess as well as evaluate research findings in a suitable manner that can be helpful to link research findings with theoretical aspects. Thus it can be stated that using both quantitative and qualitative research methods can be advantageous to make a connection between statistical findings through the survey method along with theoretical aspects of concerned research topics that is impacts of VAT system on consumers’ purchasing behaviour in Bahrain. In words of Fletcher (2017, p.185), mixed analysis method is strongly helpful to interpret research findings in a healthy manner. In this regard, it can be mentioned that survey findings become helpful to have practical data based on VAT implementation whereas the thematic secondary analysis becomes helpful to develop a sense based on changing perspectives of consumers behaviours’ due to implementation of VAT system. Hence, this research study proceeds with both primary quantitative as well as secondary qualitative data.

3.7 Data collection method

This research study has considered 150 populations for collection of primary quantitative data. In this regard, employees from Bahrain supermarket such as Alosra, Masterpoint and Jawad supermarket have been taken into consideration. In the views of Smith (2015, p.55), primary data collection method can be helpful to provide statistical findings of research topic whereas the secondary data collection method has focused to provide theoretical findings of concerned research topic. Besides, it has been estimated by the researchers that 100 numbers of employees can be turned out for participating in survey process actively. In order to proceed with the survey process willing employees are involved and they have been asked about the current way of changes in VAT system in Bahrain. In this respect, proper confidentiality has been maintained by researchers to maintain data privacy that appears helpful to complete the data collection process in an efficient manner.

Figure 3.5: Data collection method

(Source: Influenced by Kothari and Patel, 2015, p.1172)

In this regard, questionnaire has been made to collect necessary information from the employees who have actively participated in survey procedure. Questions have been formed based on 5- point Likert scale in which 1 denotes that the individual strongly disagree with concerned fact and 5 indicates that the employees strongly agreed with the concerned fact of VAT system. During the survey method questions are asked to the surveyed employees who are working in Bahrain supermarket for more than 3 years. This appears advantageous to understand changes in consumers’ purchasing behaviour in terms of implementation of VAT system.

On the other hand, secondary data is collected from a number of online journals and articles based on impacts of VAT system on consumers’ purchasing behaviour. The journals that have been published after 2015 have been taken into critical consideration to have more relevant data. Thereby, all of the relevant and authentic literary sources have been taken into consideration to understand the impacts of VAT implications on consumers’ purchasing behaviours.

3.8 Data analysis

There are two main types of data analysis named as qualitative and quantitative data analysis. As mentioned by Saunders and Bezzina (2015, p.300), selection of appropriate data analysis technique appears helpful for researchers to have most appropriate results upon completion of research study. In case of this concerned research work, non purposive random sampling technique has been taken. Thus it has been ensured that no biases have taken place in data analysis procedure. As opined by Kumar (2019, p.54), in case of non purposive random sampling, sampling numbers are selected with the help of computer random number generator. Hence, it can be stated that effective data analysis technique has been helpful for researchers to interpret findings to have a suitable conclusion based on concerned research topic.

Figure 3.6: Methods of data analysis

(Source: Influenced by Dumay and Cai, 2015, p.122)

In this research work, SPSS has been used to analyse collected data in an efficient manner. In this regard, bivariate correlation and linear regression statistical calculations have been taken into critical consideration. Besides, descriptive statistics, Chi square test, paired sample test as well as hierarchical sample analysis have also been performed by researchers. In order to perform secondary research thematic analysis has been conducted. Themes are formed based on current implications of VAT system and changes in consumers’ purchasing behaviours due to this system in Bahrain.

3.9 Validity and reliability

In every research study maintenance of validity and reliability are necessary to enhance research outcomes. As described by Hickson (2016, p.382), credibility of a research work is dependent on the reliability of collected data. In this regard, it can be stated that validity of data is critically li9nked with data reliability. As a result of this, stability of collected information has been enhanced and consistencies of research outputs are maintained at a steady state. In order to conduct a research work with greater efficiency a researcher needs to be conscious about the use of data collection method, otherwise use of same data collection technique again and again may lead to gather huge interrelated data that creates confusion during interpretation (King and Mackey, 2016, p.215).

In case of this research study, the impacts of VAT implications on purchasing behaviours of consumers have been analysed. Thus, primary emphasis has been implemented on maintenance of data reliability and validity. In order to enhance data reliability factual data has been collected from annual reports of organisations as well as collection of employees’ reviews who are working currently in Bahrain supermarkets. Along with this, journals that are published after 2015 have been taken into consideration to improve data validity. Authentic peer reviewed journals and articles are considered for increasing research credibility in an efficient manner.

3.10 Ethical consideration

Maintenance of good ethics during research study is helpful for researchers to analyse collected data in an appropriate manner. Thus, researchers of this study have maintained some ethics to complete the study in an efficient manner.

3.10.1 Maintaining rights and safety of participants

During data collection process none of the surveyed employees have been forced to reveal their confidential information about the business process. Thus rights of participants have been maintained in an efficient manner. Moreover, survey process has been conducted in an appropriate manner, so that participants feel encouraged to provide proper information about changing consumers’ behaviours due to VAT system.

3.10.2 Maintenance of research value

In order to enhance the value of research study the researchers have followed some ethics such as they have helped the participants to be involved in the survey process. It appears helpful to improve research credibility in an efficient manner.

3.10.3 Reducing harm to participants

During the survey process it has been noticed that the survey process has been helpful for surveyed employees or not. Questionnaire has been made in such as manner that is not harmful to any of the participants. Besides, concerned employees are not forced to provide information which they are not willing to reveal.

3.10.3 Informed consent

In order to carry out research work in an effective way, researchers has informed about the purpose of this study to responsible authorities. Besides, personal details of participants are kept confidential throughout the process. Thus transparency in data analysis process has been maintained in an efficient manner.

3.10.4 Maintenance of data confidentiality

A guideline of the Data Protection Act 1998 has been maintained in order to collect and analyse data (Legislation.gov.uk, 2019). Irrelevant and improper data have been excluded during data analysis process. Name and designations related information of surveyed employees have been protected by researchers in an efficient manner.

3.6 Limitations of research design

This research has faced numerous limitations in the process of its implication. The reluctant nature of customers has been identified as a barrier for collection of authentic data. Collection of authentic data has proved as the limitation of accurate execution of research study. The reluctant nature of customers has been identified as a barrier for collection of authentic data. Time and resources are also major limitations for proper execution of this research study.

According to Choy (2014, p.102), usually an effective research design needs sample size in quantity but due to lack of resources makes large scale research impossible. Particularly the developing country Bahrain, their interested parties have been lacking in skill and the resources needed to conduct through a subjective evaluation. Limitations of research in this study have related these given points:

The exact formulation of aims and objectives in this research: The objectives of this research are formulated too broadly. If the formulation of its objectives could have narrowed than the focus level of this research could be increased.

Proper implementation of methods of collection of data: Due to lack of extensive experience in the collection of Primary data, there is a significant chance of implementing the method of data collection to be inaccurate.

Lacking in the previous study of research area and limited scope discussion and the sample size: The previous studies is an important part of research, it helps to associate the work scope that has done so far in this research area. The sample size depends upon the complexion research problems and it is analysed that it is a time consuming process.

3.12 Summary

Thus it can be summarised that selection of effective methods is critically important to complete research study in an efficient manner. In this regard, this section has provided basic concepts of research methodologies that appear beneficial to collect and analyse research data in an efficient way. Besides, all types of research techniques are incorporated to provide a healthy environment for completing research study in an appropriate manner. In this regard, effective justifications have been given to explain the reasons for considering specific data analysis method, research approach, and design as well as data collection technique.

In case of this research study, positivism philosophy, inductive approach, descriptive design and both primary and secondary data analysis process have been taken into consideration. Primary data analysis has been done based on collection of employee reviews and secondary data analysis has been done based on authentic literary sources and thematic analysis.

Chapter 4: Data analysis

4.1 Introduction

Data analysis process is helpful to interpret research findings in an efficient manner. In this respect, this chapter has focused on analysing both primary and secondary research method which can help to understand perception of the employees. It has focused on primary quantitative data collection process to conduct survey with the employees of Bahrain. On the other hand, it has discussed several themes related to importance of VAT in this country. Based on four themes it has discussed significance of this.

4.2 Data analysis

4.2.1 Primary data analysis

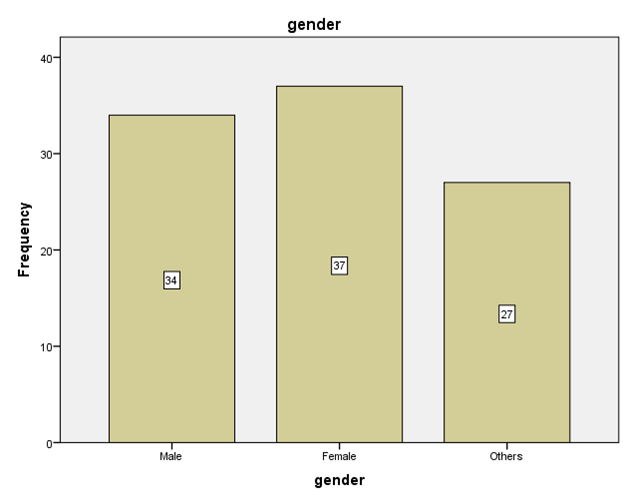

Block 1: Demographic block

1. Gender

|

gender |

|||||

|

|

Frequency |

Percent |

Valid Percent |

Cumulative Percent |

|

|

Valid |

Male |

34 |

34.7 |

34.7 |

34.7 |

|

Female |

37 |

37.8 |

37.8 |

72.4 |

|

|

Others |

27 |

27.6 |

27.6 |

100.0 |

|

|

Total |

98 |

100.0 |

100.0 |

|

|

Table 4.1: Number of Gender participants

Figure 4.1: Total Number of gender participants

Analysis

As per the observation from the above table, it can be highlighted that the number of female participants was 37 whose percentage is 37.4%. On the other hand, male participants were 34 with a valid percentage of 34.7%. However, the number of other participants was 27 with a percentage of 27.6%. Thus, the number of participants based on gender has been shown in the above table along with the justified graph.

2. The age group of the participants

|

Age group |

|||||

|

|

Frequency |

Percent |

Valid Percent |

Cumulative Percent |

|

|

Valid |

25-35 |

30 |

30.6 |

30.6 |

30.6 |

|

36-45 |

42 |

42.9 |

42.9 |

73.5 |

|

|

Above 45 |

26 |

26.5 |

26.5 |

100.0 |

|

|

Total |

98 |

100.0 |

100.0 |

|

|

Table 4.2: Age Groups of Participants

Figure 4.2: Participants age group

Analysis

On the basis of the above table, it can be assumed about the age group of the participant. However, from the mentioned table, it can be observed that 30 participants’ age was in-between 25 to 35 years. Along with 40 participants’ age was between 35 to 45 and 28 participants’ age was above 45 years. Thus, for this survey, a justified graph has been given which shows the appropriate age of the participants who have been surveyed.

a) How long have you been working in this supermarket?

|

Working experience in supermarket |

|||||

|

|

Frequency |

Percent |

Valid Percent |

Cumulative Percent |

|

|

Valid |

Less than six months |

22 |

22.4 |

22.4 |

22.4 |

|

Six months to one year |

35 |

35.7 |

35.7 |

58.2 |

|

|

One to three year |

20 |

20.4 |

20.4 |

78.6 |

|

|

Three to five year |

21 |

21.4 |

21.4 |

100.0 |

|

|

Total |

98 |

100.0 |

100.0 |

|

|

Table 4.3: Working experiences of the participants

Figure 4.3: Participants working experience

Analysis

In the above table, it has been highlighted about the working experience of the participants, in which 22 participants’ experience was less than six months. However, 35 participants experienced was in- between 6 months to 1 year, along with 20 participants experience is in- between 1 to 3 years and 21 participants experiences between 3 to 5 years who have participated in the survey. The working experiences of the participants which have been provided by them have analyzed with the help of the appropriate table as well as a graph which has provided a justified answer to the question regarding their experience.

Block 2: Measuring customer purchasing behavior

|

Statistics |

||||

|

|

Increasing VAT reduce customer purchasing intention |

Customers not willing to buy a product without urgent |

Customers offended with increasing VAT imposition |

|

|

N |

Valid |

98 |

98 |

98 |

|

Missing |

0 |

0 |

0 |

|

|

Mean |

3.1020 |

2.8980 |

2.9388 |

|

|

Median |

3.0000 |

3.0000 |

3.0000 |

|

|

Mode |

4.00 |

2.00 |

2.00 |

|

|

Std. Deviation |

1.28022 |

1.30416 |

1.33019 |

|

Table 4.4: Statistic Data on survey questions 3 to 5

|

Statistics |

||||||

|

|

Supermarket facing tremendous loss |

VAT imposition reduced customer arriving at the supermarket |

Increasing VAT affected sales margin of supermarket |

Bahrain law effecting in the country economy |

The imposition of tax by Bahrain law betterment of mankind in Bahraini |

|

|

N |

Valid |

98 |

98 |

98 |

98 |

98 |

|

Missing |

0 |

0 |

0 |

0 |

0 |

|

|

Mean |

3.2347 |

3.0204 |

3.1020 |

3.0306 |

2.8163 |

|

|

Median |

3.5000 |

3.0000 |

3.0000 |

3.0000 |

3.0000 |

|

|

Mode |

4.00 |

4.00 |

4.00 |

3.00 |

2.00 |

|

|

Std. Deviation |

1.37579 |

1.38460 |

1.37346 |

1.33512 |

1.35728 |

|

Table 4.5: Statistic Data on survey questions 6 to 10

3. The increasing VAT has reduced the purchasing intention of the customers

|

Increasing VAT reduce customer purchasing intention |

|||||

|

|

Frequency |

Percent |

Valid Percent |

Cumulative Percent |

|

|

Valid |

Strongly disagree |

12 |

12.2 |

12.2 |

12.2 |

|

Disagree |

24 |

24.5 |

24.5 |

36.7 |

|

|

Neutral |

19 |

19.4 |

19.4 |

56.1 |

|

|

Agree |

28 |

28.6 |

28.6 |

84.7 |

|

|

Strongly agree |

15 |

15.3 |

15.3 |

100.0 |

|

|

Total |

98 |

100.0 |

100.0 |

|

|

Table 4.6: Responses about customer purchasing intention

Figure 4.4: Responses for customer purchasing intentions

Analysis

In the above table, the survey has been done by asking participants about the expansion of the VAT have decreased the intentions of the customers for buying products. In this survey, 98 participants have surveyed for understanding their opinion from which 12 participants have responded strongly disagreed, 24 participants have their response to disagree. However, 19 participants have provided neural responses along with 28 participants’ have agreed from the above statement and 15 have responded as strongly agreed. However, in wider note, commented Šálková et al. (2017, p.1045), that the increase of the VAT on the products has restricted the customers from buying anything as they have to provide huge amount of tax for the product purchase. Thus, it can be assumed that the enhancement of the VAT is the purchasing behavior of the customers for which 28 participants have responded by agreeing to the statement (Kour et al. 2016, p.17). Thus, it can be stated that the application of the VAT is affecting the purchasing behavior of Bahrain for which a high number of participants have agreed. The VAT system can impact the purchasing attitude of the customers in a negative as well as positive way (Ramdhani et al. 2018, p.224)

4. The customers are not willing to buy a product without urgent need

|

Customers not willing to buy a product without urgent |

|||||

|

|

Frequency |

Percent |

Valid Percent |

Cumulative Percent |

|

|

Valid |

Strongly Disagree |

15 |

15.3 |

15.3 |

15.3 |

|

Disagree |

30 |

30.6 |

30.6 |

45.9 |

|

|

Neutral |

16 |

16.3 |

16.3 |

62.2 |

|

|

Agree |

24 |

24.5 |

24.5 |

86.7 |

|

|

Strongly agree |

13 |

13.3 |

13.3 |

100.0 |

|

|

Total |

98 |

100.0 |

100.0 |

|

|

Table 4.7: Responses regarding customer buying behavior

Figure 4.5: Responses for customer attitude for purchasing a product

Analysis