QUESTION

Assignment 2 : 1200 words excluding refernces cover page

ASSIGNMENT 1: COMPARE AND CONTROL COSTING SYSTEM

Table of Contents

Introduction

Different types of costing system

The comparison and contrast between the costing system

Identification of advantages and disadvantages of costing system

Utilization of the costing system by the organization

Conclusion

Reference list

Assignment 1

Introduction

Implementation of proper costing system is helpful for understanding the amount of investment along with the amount of profit of an organization. The costing system is designed to monitor the costs and makes analysis on revenues, costs and profitability. In this part, various costing system, their various advantages and disadvantages along with the appropriate application of costing system in respect to the concerned organization namely ABS lubricant are analysed here.

Different types of costing system

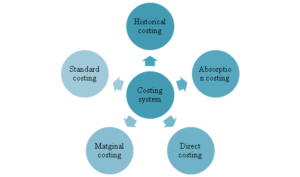

The cost accounting system is taken as the framework for estimating the costs of products of an organization. As mentioned by Ahadi & Azar (2016), estimation of accurate costs for products is critically important for preceding various profitable operations on the part of the organization. The various types of costing system that can be applied in an organization are as follows-

-

Historical costing

In this case, the aim of the costing system is to ascertain costs that are incurred in past. This type of costing system is used in post-mortem examination of the exact cost as well as assuming the actual figure of costs based on the performance level.

-

Absorption costing

As described by Almeida & Cunha (2017), this costing system is used in fixing the manufacturing overheads that are allocated to products as well as the analysis of stock valuation.

-

Direct costing

In this type of costing method the product is subjected to charge according to the variation in volume. Besides, the indirect cost system is neglected for inventory valuation.

-

Marginal costing

In this type of costing system the cost is divided into fixed and variable costing. The marginal costing system focuses on recovery of fixed cost before contributing to operational profit (Dale & Plunkett, 2017).

-

Standard costing

The use of standard costing system is specific for accounting, evaluating stock and fixing selling prices. In words of Machado et al. (2015), when the costs of products are predetermined in respect to any operating conditions, it is called as standard costing.

Figure 1: Different types of costing system

(Source: As influenced by Ogilby, Pforsich & Johnstone, 2016)

The comparison and contrast between the costing system

Comparison

- All of the costing system applied for determining the appropriate values of products and thereby all of the systems deal with the development of product value.

- The costing system is affected by the change in product volume (Yigitbasioglu, 2016).

- Most of the costing systems are effective in accommodating the changing conditions in organizations.

- They focus on current business trends and budget range.

- Most of the costing system focuses on proper planning and allocating overhead expenses (Ahadi & Azar, 2016).

Contrast

-

The historical costing method focuses on the predetermined costs of various products whereas the direct costing method focuses on the cost of products depending on their volume.

-

The absorption costing focuses on analysis on stock valuation whereas the marginal costing method focusing on recovery of predetermined costs.

-

The standard costing procedure focuses on fixing of selling price and the marginal costing emphasizes on variation in selling price (Dale & Plunkett, 2017).

Identification of advantages and disadvantages of costing system

The above mentioned costing system has several advantages and disadvantages while applying them into business structure. In the view of Tuccillo (2016), the advantages and disadvantages are mentioned as follows-

|

Different costing systems |

Advantages |

Disadvantages |

|

Historical costing |

|

|

|

Absorption costing |

|

|

|

Direct costing |

|

|

|

Marginal costing |

|

|

|

Standard costing |

|

|

Table 1: Advantages and disadvantages of various costing systems

(Source: Influenced by Tuccillo, 2016)

Thereby, considering all the advantages and disadvantages of different costing system an organization decides to incorporate the most effective costing strategy which focuses on the overall development of their business.

Utilization of the costing system by the organization

An organization generally focuses on implementation of appropriate costing strategy for managing their resources and developing the business process in an effective manner. The organization namely ABS lubricant emphasizes on producing lubricants for all types of vehicles such as car, bike or any types of machinery. The authority also focuses on producing grease product by involving specialist lubrication technology (Abslubricants.com, 2019).

In order to meet the market demand the company management focuses on implementing the standard costing system for managing the resources in an efficient manner. As mentioned by Machado et al. (2015), the authority of a developing organization tries to incorporate such s costing strategy which is beneficial enough for having the required amount of profit. Hence, the authority of ABS lubricant focuses on the standard costing system for the long term sustainable growth of their organization.

This costing system is advantageous for them through the following ways-

-

Management by expectation

This effective costing system helps the management to focus on those items which have no use at all. Hence, time is saved and various value added activities are given equal importance.

-

Reducing cost

The standard costing system emphasizes on the thorough setting, revision and monitoring the resource quantity which, in turn, helps the authority to incorporate various modern techniques to produce various lubricants and grease (Abslubricants.com, 2019).

-

Effective pricing

This costing method focuses on the calculation of total cost for producing various synthetic lubricants and determination of accurate selling price.

-

Focusing on inventory valuation

The implementation of standard costing method makes the inventory valuation easier as it gives equal importance of various physical units (Tuccillo, 2016).

-

Cost control management

The effective incorporation of cost control method is helpful for the organization to understand the deviation of prices of various lubricants and helps to decide whether it is favourable or unfavourable.

-

Management of healthy budget

Standard costing system helps to calculate the budget only by following the formula

Budgeted Cost = number of output units x Standard Cost per unit.

Conclusion

Thus it can be concluded that effective implementation of costing system can be helpful to manage resources and have the required amount of profit from the business process. Thus analysis of various advantages and disadvantages of a number of costing methods is helpful for sustainable growth of an organization. In this respect, it has been seen that the ABS lubricant organization has focused on implementation of standard costing system. It helps the authority to manage resources and set their budget limits for effective growth of the organization as a whole.

Reference list

Ahadi, A., & Azar, S. F. (2016). The study of the possibility of using activity-based costing system (ABC)(Case Study: General Directorate of Roads and Urban Development of East Azerbaijan Province). International Academic Journal of Accounting and Financial Management, 3(6), 1-8. Retrieved on: 22/1/2019. Retrieved from: http://iaiest.com/dl/journals/5%20IAJ%20of%20Accounting%20and%20Financial%20Management/v3-i6-jun2016/paper1.pdf

Almeida, A., & Cunha, J. (2017). The implementation of an Activity-Based Costing (ABC) system in a manufacturing company. Procedia manufacturing, 13, 932-939. Retrieved on: 22/1/2019. Retrieved from: https://ac.els-cdn.com/S2351978917307990/1-s2.0-S2351978917307990-main.pdf?_tid=aaecd39c-94dc-406e-81cb-120fbbff06de&acdnat=1549266748_3c1c21b12723f9db3ead3b583606fc4f

Abslubricants.com (2019). ABS lubricants. Retrieved on 22/1/2019. Retrieved from: http://abslubricants.com

Dale, B. G., & Plunkett, J. J. (2017). Quality costing. Abingdon: Routledge. Retrieved on: 22/1/2019. Retrieved from: https://www.taylorfrancis.com/books/9781351907286

Machado, A., Mendes, C., da Silva, M. M., & Almeida, J. (2015, April). Costing as a Service. In ICEIS (3) (pp. 173-181). Retrieved on: 22/1/2019. Retrieved from: https://fenix.tecnico.ulisboa.pt/downloadFile/563345090412738/dissertacao.pdf

Ogilby, S. M., Pforsich, H., & Johnstone, T. (2016). Activity-Based Costing/Management: Lessons from a Public Service Organization. The Journal of Government Financial Management, 65(4), 32-48. . Retrieved on: 22/1/2019. Retrieved from: https://www.questia.com/library/journal/1P4-2101837659/activity-based-costing-management-lessons-from-a

Tuccillo, D. (2016). Activity-Based Costing in Public Services. Global Encyclopedia of Public Administration, Public Policy, and Governance, 1-6. Retrieved on: 22/1/2019. Retrieved from: https://link.springer.com/referenceworkentry/10.1007%2F978-3-319-31816-5_2318-1

Yigitbasioglu, O. (2016). Firms’ information system characteristics and management accounting adaptability. International Journal of Accounting and Information Management, 24(1), 20-37. Retrieved on: 22/1/2019. Retrieved from: https://eprints.qut.edu.au/87535/1/IJAIM_Ogan%20%282%29.pdf

ASSIGNMENT 2: TOTAL QUALITY MANAGEMENT

Table of contents

Table of contents

Introduction

Issues

Impact of the issues

Possible Changes

Present statement of the company

Conclusion

References

Introduction

Quality of product and service is one of the major factors that influence the organisational performance. This study aimed to evaluate the quality management issues faced by GM Holden, a car manufacturing organisation. It will illuminate the issues in this context faced by the organisation as well as their impact on the organisational performance. Along with that, the study will highlight the current state of the company because of the major challenge faced by the organisation. Along with the probable strategies will be highlight which would have been facilitating for the company to reduce the ill-effect of that issue.

Issues

GM Holden has faced certain issues regarding the quality of their cars. In terms of quality, their cars have been identified with safety issue as well as lower technologies. Cars manufactured by GM Holden was emitting more carbon dioxide than it was required which was hazardous for the environment and was also dangerous for the life of the people. This was caused due to the poor performance of the employees as well as due to use of lower technologies. The employees working at GM Holden were not efficient and ignored the quality of the materials used. In order to experience higher profits, the company used poor quality products. People who purchased this car faced lots of difficulties while using these cars. These cars required more fuel than others. These cars were increasing global warming at a high rate. Another issue was the unsafe vehicles manufactured by GM Holden (GM quality manager warned board of serious problems in 2002, 2019). This hampered the goodwill of the company and lost trust relationships with many customers. The major issue of these cars were that these cars were unsafe for people and could even cause health issues to people. People started hating its cars and stopped purchasing it. As a result, sales of these cars were decreased and this caused a negative impact on the people.

Impact of the issues

These issues have influenced the organization severely. Regarding the organisational performance, such issue of safety and technology put a negative impact on the market. As a result, financial statement of GM Holden has been influenced negatively immediate after the issues. This not only creates the challenges o regarding the product quality, but also put a question on the approach of the company. As a result customers find themselves detached from this car manufacturing organisation. These quality issue have been identified at the end of 2002 and the negative impact has been identified in terms of financial statement of 2004 (Annual Report 2004. 2019). This has been identified that, GM Holden has received a negative curve in terms of its income from continuous operation, margin of net profit as well as earning per share in terms of continuing operations. It has been identified that the company has profit margin of the company reach at 1.4% from 1.5% in 2003. Net income has also been reduced to $ 2805 million from $ 3822 million (Annual Report 2004. 2019). This has been continued in next year’s also. Along with that, these issues have influenced the liabilities of the company. In 2004, liabilities of the company have been increased from previous years because of the ill-effect of such quality issues. In 2003, liabilities of the company were $ 73930 million which has been marked at $ 77727 million in 2004. As the organisation has faced the challenge of low quality of technologies, they have been forced to apply advanced technologies which influence the cost of production in next year’s. This was also responsible for the reduced financial performance of the company. In order to manage those issues of low safety level and technology, GM Holden has been forced to improve its cash investments in 2004. In 2003, cash in investment was $ 36117 million which has been turned into $ 50848 million in 2004 (Annual Report 2004. 2019).

Possible Changes

Implementation of TQM model could have helped the company in avoiding the consequences of producing poor quality product. With the use of TQM model the company could have consulted with its top level managers and could have known about the needs of the customers and satisfied them. According to Carmona-Márquez et al.(2016), application of TQM model could allow an organisation to reduce its cost in an organising way. This could facilitate the company to reduce its liabilities faced as result of those quality issues. TQM model helps a company in strategy making considering the quality development (Nallusamy, 2016). GM Holden could have started using advanced technology products in order to avoid its problems. It could have exchanged its poor products with good quality products in order to regain its financial position back in the market and to gain customer satisfaction. It could have lowered its car price in order to attract more customers and regain customer trust. It could have started using products which emitted lower amount of carbon-dioxide gas in order to safeguard the life of the people. The company could have improved the efficiency as well as performance of the employees. As GM Holden suffered a lot regarding the safety of people and using poor quality products, it lost many customers and also started having trust issues with people. So, in this regard GM Holden tried to overcome and recover its position in the market. The company tried to find out the reason for producing such poor product and tried to change the poor material that was used before. GM Holden started importing different type of car materials from different countries. GM Holden also focused on using car materials which did not emit much carbon-dioxide gas in order to save the environment and the people. It also started buying best products and used those products in the cars. This was a big challenge for GM Holden to recover its position back.

Present statement of the company

Though the company has improved its performance, and still continuing its venture after that challenge, they have vastly affected by those issues. Net sales and revenue of the company is $ 145588 million in 2017 (Annual report of GM holden 2017, 2019). This can be identified as below the level of 2002. It has also faced challenges to maintain its market share and customers as result of that quality issue. This also forced the company to reduce its range of productions in order to reduce its production costs as well as liabilities. These issues and present state of performance also suggests that the strategies adopted by the company was not enough effective to resolve the challenges generated by the quality management issues. However, those strategies cannot be denied as completely ineffective as the company is still able to manage a significant market share in spite of the challenge and downturn. The major impact has been identified in cost management which have been still generating challenges for the company.

Conclusion

Thus it can be concluded that, product quality has influence the organizational performance in terms of GM Holden. Unsafe vehicles of GM Holden have negatively influenced the organisational performance. However, the organisation has successfully resolved the immediate effect and back in positive numbers. This study has also highlighted the probable strategies for the companies in this context. Application of Total Quality management could have been an effective strategy for the company to manage those quality issues effectively.

References

Annual Report 2004. (2019), annualreports.com. Retrieved on: 1st february 2019. Retrieved from: http://www.annualreports.com/HostedData/AnnualReportArchive/g/NYSE_GM_2004.pdf

Annual report of GM holden 2017. (2019), annualreports.com. Retrieved on: 1st february 2019. Retrieved from: http://www.annualreports.com/HostedData/AnnualReports/PDF/NYSE_GM_2017.pdf

Carmona-Márquez, F. J., Leal-Millán, A. G., Vázquez-Sánchez, A. E., Leal-Rodríguez, A. L., & Eldridge, S. (2016). TQM and business success: do all the TQM drivers have the same relevance? An empirical study in Spanish firms. International Journal of Quality & Reliability Management, 33(3), 361-379. Retrieved on: 1st february 2019. Retrieved from: http://eprints.lancs.ac.uk/74393/1/151007_Paper_IJQRM_vfinal.pdf

GM quality manager warned board of serious problems in 2002. (2019), autonews.com. Retrieved on: 1st February 2019. Retrieved from: https://www.autonews.com/article/20140620/OEM11/140629972/gm-quality-manager-warned-board-of-serious-problems-in-2002

Nallusamy, S. (2016). A proposed model for sustaining quality assurance using TQM practices in small and medium scale industries. In International Journal of Engineering Research in Africa .22. 184-190 Retrieved on: 1st february 2019. Retrieved from: https://www.researchgate.net/profile/Dr_Nallusamy/publication/295074288_A_Proposed_Model_for_Sustaining_Quality_Assurance_Using_TQM_Practices_in_Small_and_Medium_Scale_Industries/links/5775ed9b08ae4645d60bb17d/A-Proposed-Model-for-Sustaining-Quality-Assurance-Using-TQM-Practices-in-Small-and-Medium-Scale-Industries.pdf

Looking for best Operation Management Assignment Help. Whatsapp us at +16469488918 or chat with our chat representative showing on lower right corner or order from here. You can also take help from our Live Assignment helper for any exam or live assignment related assistance.