QUESTION

Submit a completed critical essay to your instructor that includes the following:

- Abstract (summarize and briefly discuss the problem, analysis, and findings)

- Introduction

- Problem Statement

- Analysis and Findings

- Conclusions and Recommendations.

Based on your analysis, what are your recommendations for the country’s leaders and creditors?

Include a description of your approach to the issues and your solutions to the problems described in the case.

Your project should meet the following requirements:

- Be 15-20 pages in length, including the supporting tables, as necessary

- Cite a minimum of three reference

ANSWER

Contents

Abstract

Introduction

History of the Greek Economic Crisis

Major factors that led to Greece’s Debt

Recent Developments and the current situation

A Path Forward: Conclusion and Recommendations

Appendix

References

Abstract

Greece has been a subject of concern for IMF (International Monetary Fund) and the European Union for quite a long time. It all started with the misrepresentation of the GDP growth rate for entering the Euro zone, and then taking low-interest loans for boosting the public sector. They did not adopt accrual accounting and reported their debt in face value terms because of their Maastricht treaty signed during the Euro membership. After the Global Financial Crisis of 2008 and the newer government formation in 2009, it was all evident that Greece has been on a continuous decline as an economy, and its debt has increased exponentially. In 2010, IMF and the European Union decided to boost the Greek economy and avoid its default by providing financial assistance. This assistance was on the condition of certain austerity measures in Greece, which they had to accept, and several reforms got introduced such as increased taxes, pension cuts, labour wages, and many more. This worsened the situation and affected their unemployment rate. There was political and social turmoil in the whole country and brain drain became a common phenomenon. The further two bail-outs provided by IMF and EU were in 2015 and 2018 respectively for boosting the financial situation, with a total support of around 300 billion euros. The Greece economy has showed positive signs of growth over last 2-3 years and the financial support has now been ended. This is a liberating time for the economy, which would decide their future in both short and long terms. Greece needs to prove that their debts are sustainable, and they need to continue taking stringent measures along with providing moral support to their citizens.

Introduction

With the third and last Economic Adjustment Programme ending for Greece in August 2018, now is the most important time for the country to take revolutionary measures in the policy and prepare both short-term and long-term plan of dealing with their long-lasting debt scorecard. The implementation of prudent fiscal policies by the Greek government along with an ambitious growth strategy are going to be the key ingredients for their debt sustainability.

Greece has been crumbling economically and financially for several years and this deterioration has been a result of their policy uncertainty, improper currency controls, lack of foreign investment and many similar things. However, the root cause for this crisis lies in their profound structural economic inefficiencies borne during 1980s. The embarkment of the country on a public sector-led economic boom has sowed the seeds of this crisis. The opportunity of Eurozone membership was not properly utilized by the Greek government and they mistook it by expanding their public-sector policies based on the artificially created low borrowing costs.

There have been three rounds of financial assistance (in 2010, 2015, and 2018) provided to the Greek government by the Eurozone government and the International Monetary Fund put together and they have fuelled more than 300 billion euros till date. These debts over the years have helped the Greek government, but they are still to become a self-sustaining government despite of these bailouts and some structural reforms such as reductions in government spending and increase in tax revenues.

For improving its financial and economic situation, Greece should focus on main areas such as Labour market inefficiencies, Public sector’s contribution to economy, Investment and Business scale opportunities, Judicial system. These improvements can make the Greece debt as sustainable in the future with a promising growth.

History of the Greek Economic Crisis

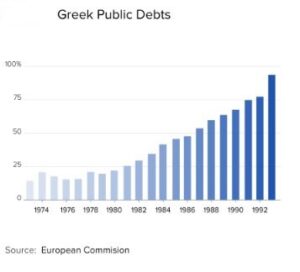

The Economic Crisis for Greece has been in the news for quite a long time. It has been created over decades of years and now it has become worst for the Greek government. It started during the latter part of 1900s itself, when Greece democratically elected government and they become the member of European Economic Community under their Common Market policy. During this period, Greece continued on its path of fiscal expansion and debt-funded growth, resulting in an exponential increase of Greek Public Debts as shown in the below given figure –

In 1992, European Union was formed along with their fiscal convergence criteria of adopting single currency i.e. Euro as their common currency by the Economic and Monetary Union. In 1999, Euro currency was launched, and the member countries had to adopt it as their common currency, based on some fiscal criteria which was also known as Maastricht criteria: –

- The inflation of the member country should be below 1.5 percent,

- The budget deficit of the member country should be below 3 percent,

- Debt to GDP ratio for the member country should be below 60 percent,

- The member country must have achieved exchange-rate stability for at least two years within their defined permitted levels of fluctuation.

Greece failed to meet some of these criteria then in 1999 and hence, was denied the membership of Euro zone in 1999. Their public-sector borrowing was also higher than the normally permitted amount, which displayed them as a weaker economy. For fulfilling these norms, Greece misrepresented its finances in 2001 and showed their budget deficit well over 3 percent. European Union also showed some leniency towards Greece and allowed them to become a member despite of their weaker financial market situation, and their currency got changed from Greek Drachma to Euro. Later in 2004, they started displaying their real budget deficit and showed the hosting of Olympic games as the major reason behind that with costs in excess of 9 billion euros, but their previous press reports proved that their budget deficit never fell before 3 percent since 1999. However, due to this public borrowing for hosting Olympic games, their budget deficit rose to 6.1 percent and debt-to-GDP ratio to 110.6 percent by 2004, which placed them under fiscal monitoring by the European Union in 2005.

Shipping and Tourism have been two major revenue generating businesses for Greece. But back in 2008, when the U.S subprime mortgage market collapsed, and Lehman brothers fall, these two departments got severely hurt and their borrowing costs increased along with financing being dried up, which built a mounting debt for the country. In 2009 when Papandreou won elections, he revealed that the Greece’s budget deficit was hovering around 12 percent, which was further revised to around 15 percent. This led credit rating agencies to downgrade Greece’s sovereign debt to junk status in early 2010 and consequently, the borrowing costs for the country spiked.

From 2010 onwards, there has been a vicious circle of debts and interests for Greece. For avoiding default, they took loans over the years, and as loans increased, their interests and loan repayments also increased. But since the country was not allowed to print their own currency notes, they were not able to repay their debts, which led them to further loans.

Major factors that led to Greece’s Debt

Though there had been numerous reasons behind the Greece’s debt, but it can be categorized under four major reasons as discussed below: –

- 2010 Bailout program by IMF along with demands for excessive fiscal adjustment:

Greece was allowed financial assistance by IMF and European Commission for avoiding their default case. But this assistance came with some stringent changes in their fiscal policy. This bailout of 110 billion euros in 2010 was aimed towards offering a safe emergency exit to private bondholders who wanted to reduce their exposure to Greek bonds. The MoU was designed to rescue the private creditors of the country, especially banks. But this affected the investment in the Greek industries, and the fiscal austerity measures in terms of low government spending and increased tax-cuts further aggravated the situation.

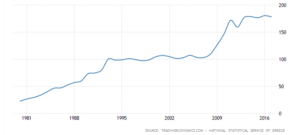

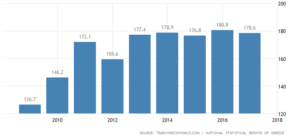

As a result of this, their Debt-to-GDP ratio increased drastically, and kept on increasing ever since then.

From the above graph of Debt-to-GDP ratio (in percent) for Greece, it can be seen that the curve has increased exponentially between the years 2010 to 2012 and then, it has remained around 170s (percent) for quite a few years [See Fig 1 in Appendix].

- Financing support provided not repaying Foreign banks properly:

The debt restructuring was delayed by 2 years due to cautionary reasons with Lehman brothers fresh in memory. Portion of the amount in 2010 was used to pay short-term creditors, and to replace those private debts by an official debt. Greek banks and other Greek financial institutions were more benefitted from this as they held one-third of the total debt. This led to substantial reduction of the fund in 2012 as the foreign investors were not completely off the hook. This affected the pre-planned funding and repayment structure of the Greece government.

- Poor structural reforms and fiscal austerity leading to an economic depression:

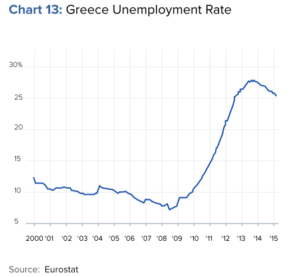

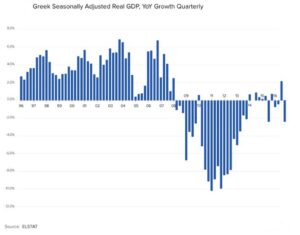

Greece had a history of poor structural reforms even before the Global Financial Crisis of 2008. But, the bail-out program and its austerity measures proved to be worse than its previous reforms. The tax administrative was reformed with increased taxes, pension system was reformed, the government spending was cut, and many other reforms were introduced. These reforms were further boosted by Grexit fears and low business confidence, which led to a drastic increase in the unemployment rate.

From the above graph, it is evident that these reforms after 2010 bail-out increased the unemployment rate and hence, the GDP growth rate also got affected as shown in Fig 2 & 3 in the Appendix section.

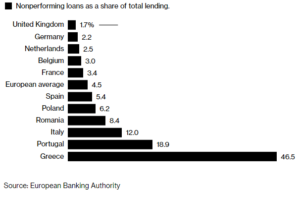

- Repeated mistakes by the creditors:

The creditors, whether it be IMF or The European Commission or the private investors, have repeatedly committed the same mistake of overlooking the intricate delicacies with the financial system of Greece. They decided to provide financial support and introduce some austerity fiscal measures without even knowing the inner working system of Greece. Private investors kept on lending the Greece government without proper background check so that they earn huge interests from those loans. For avoiding defaults and repaying loans from private investors and other institutions, Greece further lend money along with three bail-outs provided by IMF and the European Commission.

The above figure gives a clear representation of how Greece has become the master of risky lending, and this has become possible only with the help of ignorant creditors.

Recent Developments and the current situation

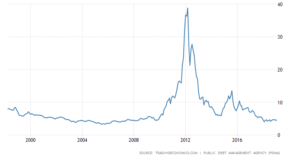

Greece has recently performed well enough to bring back its GDP growth rate into positive percentage. Though there had been several disputes between the political parties after the 2015 bail-out on whether to grant further financial assistance or not, because the stringent norms were necessary to follow according to the MoU. Greece has announced historical tax reforms, cut public spending, privatized public assets, and reformed labour laws in a completely coherent manner for a collaborative growth of the nation. This recent development in the value of Greece Government 10-year bond yield chart can be seen by the figure shown below:

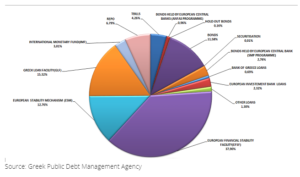

Greece has recently exited its bailout programme in August 2018 and their nine years of reliance on huge loans from international finance bodies along with stringent budget cuts have ended. Along with the third bail-out programme, the Euro zone has allowed some leniency to the Greece government for repayment of its loans under which, Greece will not have to pay any of its money until 2032 – which is a representation of a 10-year extension in the maturities of its debt and, all the euro zone members will again assess the situation in 2032 and then decide upon the further measures needed to make the Greece’s debt pile as sustainable. This is a very important step for Greece as their major chunks of debt are held by European Commission (EFSF and ESM), IMF, and GLF [See Figure 4 in Appendix].

Currently, ECB and other central banks are buying bonds from euro zone countries as a part of strengthening the economic measures. The latest debt relief measure provided by Euro zone enforces any profits made by central banks in the euro zone on Greek bonds to return to Athens in two equal tranches every year from 2018 to 2022. They no longer have to implement structural reforms as demanded by creditors in lieu of their funds provided. As of now, due to these debt reliefs, Greece can claim to have some financial stability and assure their citizens of development.

Due to these measures, IMF sees Greek debt repayments as no concern in the medium term. However, they are still doubtful about the Greece’s repayment and financial capabilities in the longer term.

A Path Forward: Conclusion and Recommendations

The debt relief measures will provide support to the Greek economy and the last cash buffer of 24 billion euros would cover their sovereign financial needs for the next 2 years. Though the Greece government has shown positive signs of growth, but they need to continue boosting their capital and cutting taxes along with cutting unsustainably high pension spending, which would lead to its substantial broadening of its very narrow tax base presently. Their GDP has expanded from last year, and export growth has been recorded in the refining oil. But still, for achieving large primary fiscal surpluses, the taxes should be increased, which is currently around 46% for personal income. The government also needs to build a proper communication channel with the citizens as the large tax rates and more pension cuts are making them hopeless thinking of the current situation as a blind tunnel with no end.

The recent analysis by IMF has showed that the debt relief package provided by Euro zone to Greece would result in initial decline of their Debt-to-GDP ratio, but it is likely to get an uninterrupted rise from around 2038. The country’s gross financing needs is also expected to breach 20 percent of its GDP by 2038, which has been set as a threshold limit by the euro zone itself. Now, the short and medium term being seen as the stable ones, the Greece government should also look towards the longer term. They should introduce an automatic mechanism linking future debt service to non-policy related factors such as GDP shocks, which would help in addressing vulnerability to shocks from the current time. This incorporation of symmetric adjustments to debt service would provide protection to both debtors and creditors, in the case of any GDP shock. This is very important for the Greece government because as of now, the Greece bonds and the Greece financial market are more prone to damage in case of any shocks in the Euro zone.

Appendix

Figure 1. Greece Debt-to-GDP ratio (in percentage)

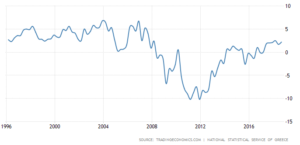

Figure 2. Greece GDP YoY growth rate

Figure 3. Greece GDP Annual Growth Rate

Figure 4. Sources of Greece’s National Debt

References

1. Jan Strupczewski, 2018 Jul 31, IMF says Greek debt sustainable medium-term, long-term uncertain, Reuters

2. Yannos Papantoniou, 2017 Jun 12, How long will the Greek crisis last, Carnegie Europe

3. Chavon Sutton, 2010 Apr 27, S&P downgrades Greek debt to junk status, CNN Money

4. Helena Smith, 2010 Nov 15, Greek deficit much bigger than estimate, The Guardian

5. Michele Kambas, 2018 Aug 29, Is Greece out of the woods, BBC News

6. Kimberly Amadeo, 2018 Nov 08, Greek Debt Crisis explained, The Balance

7. Silvia Amaro, 2017 Feb 09, Should Greece stay, or should it go? Analysts divided on whether Greece will exit euro, CNBC

8. Rebecca M. Nelson, 2017 Apr 24, The Greek Debt Crisis: Overview and Implications for the United States, Congressional Research Service

9. Olivier Blanchard, 2015 Jul 10, Greece: Past critiques and the path forward, Vox EU

10. Solon Molho, 2017 Dec 13, The Greek Debt Crisis explained, Toptal

11. Ferdinando Giugliano, 2018 Jun 18, Why Three Rescues Didn’t Solve Greece’s Debt Problem, Bloomberg

12. Katya Adler, 2018 Aug 20, Greek bailout crisis in 300 words, BBC News

13. Sybren Kooistra, 2010 Mar 19, Overcoming the Greek debt crisis and organizing the future of the European monetary union, European Greens

14. Barry Eichengreen, 2018 Mar 20, Putting the Greek debt problem to rest, Vox EU

15. Neil Gallagher, 2004 Nov 15, Greece admits fudging euro entry, BBC News UK

16. Danae Kyriakopoulou, 2017 Mar 26, Assessing Greek Debt sustainability, OMFIF

17. IMF European Department, 2016 May 23, Greece: Preliminary Debt Sustainability Analysis-Updated Estimates and Further Considerations, International Monetary Fund (IMF)

18. Matt Steinglass, 2009 Dec 17, Papandreou tries to prop up the pillars, The Economist

19. Karen Sparks, 2004 Dec 31, Criteria for joining the Euro zone, Encyclopaedia Britannica

Looking for best Finance Assignment Help. Whatsapp us at +16469488918 or chat with our chat representative showing on lower right corner or order from here. You can also take help from our Live Assignment helper for any exam or live assignment related assistance.