QUESTION

Report should be 3 pages, and applying material from the chapter readings of this module, with APA Style and answer the above questions. Integrate references (minimum of 6). Reply to these questions in essay (not Q & A) format.

1. Estimate the current profit figures of SLS from December 2012 to May 2013 to evaluate the viability of the business. 2. Examine SLS’s break-even point for May 2013. 3. Estimate the profitability of conducting each type of yoga class – i.e. group classes, private classes, and “salt cave” classes. 4.Consider the implications of the analyses above for SLS. 5.Conduct sensitivity analyses based on different scenarios of rental costs, fees paid to yoga teachers and pricing. 6.Recommend a plan of action for the owners of SLS.

Please take a look into the attached excel sheets to collect the stats and draw graphs where needed.

here is hints for the question above: https://prezi.com/p/vtyyi4k1zfsu/space-light-studios-cost-volume-profit-analysis-the-business-of-yoga-case-specification/

Sheet 1

| Space & Light Studios: Cost-Volume-Profit Analysis and the Business of Yoga Teaching Note |

| Chua Wei Hwa, Koh Wei Chern & Wee Beng Geok |

| Publication No: ABCC-2014-002(TN) |

| HBP No. NTU062 |

| Business Viability.xls |

| COPYRIGHT © 2015 Nanyang Technological University, Singapore. All rights reserved. No part of this publication may be copied, stored, transmitted, altered, reproduced or distributed in any form or medium whatsoever without the written consent of Nanyang Technological University. |

NTU062-xls-ENG xlxs

Dec 2012

| Main Sources of Revenue | # of client visits | Revenue per class | |||||||

| Private | 7 | 130 | 910.00 | ||||||

| Group Classes | 296 | 10 | 2,960.00 | ||||||

| TOTAL REVENUE | 3,870.00 | ||||||||

| LESS: | |||||||||

| Monthly rental | 1900 | Median rental. 5.89 | 11,191.00 | ||||||

| No bus fees till April 2013. Monthly shared administrative fees | 3,500.00 | ||||||||

| Monthly MBO fees | 70 | Exchange rate for US$.1.25 | 87.50 | ||||||

| (14,778.50) | |||||||||

| LESS: | |||||||||

| Group classes cost | No of classes | Fees Paid to Teacher | 112 | Known average rate paid to yoga teacher per class. 60.00 | (6,720.00) | ||||

| LESS: | |||||||||

| Private classes cost | No of classes | Fees Paid to Teacher | 7 | 60.00 | (420.00) | ||||

| TOTAL COSTS | (21,918.50) | ||||||||

| NET PROFIT FOR GROUP/PRIVATE/SALT CLASSES FOR THE MONTH | (18,048.50) | ||||||||

Jan 2013

| Main Sources of Revenue | # of client visits | Revenue per class | |||||||

| Private | 21 | 130.00 | 2,730.00 | ||||||

| Group Classes | 1009 | 10.00 | 10,090.00 | ||||||

| Salt Stretch | 18 | 70.00 | 1,260.00 | ||||||

| TOTAL REVENUE | 14,080.00 | ||||||||

| LESS: | |||||||||

| Monthly rental | 1900 | 5.89 | 11,191.00 | ||||||

| Monthly shared administrative fees | 3,500.00 | ||||||||

| Monthly MBO fees | 70 | 1.25 | 87.50 | ||||||

| (14,778.50) | |||||||||

| LESS: | |||||||||

| Group classes cost | No of classes | Fees Paid to Teacher | 137 | 60.00 | (8,220.00) | ||||

| LESS: | |||||||||

| Private classes cost | No of classes | Fees Paid to Teacher | 21 | 60.00 | (1,260.00) | ||||

| LESS: | |||||||||

| Salt-cave classes cost – teachers | No of classes | Fees Paid to Teacher | Assume all salt-cave classes have equal no. of clients. Therefore, rental is $35 per class.6 | 60.00 | (360.00) | ||||

| Salt-cave classes cost – rental | No of classes | Rental per Class | 6 | 35 | (210.00) | ||||

| TOTAL COSTS | (24,828.50) | ||||||||

| NET PROFIT FOR GROUP/PRIVATE/SALT CLASSES FOR THE MONTH | (10,748.50) | ||||||||

Feb 2013

| Main Sources of Revenue | # of client visits | Revenue per class | |||||||

| Private | 15 | 130.00 | 1,950.00 | ||||||

| Group Classes | 699 | 15.00 | 10,485.00 | ||||||

| TOTAL REVENUE | 12,435.00 | ||||||||

| LESS: | |||||||||

| Monthly rental | 1900 | 5.89 | 11,191.00 | ||||||

| Monthly shared administrative fees | 3,500.00 | ||||||||

| Monthly MBO fees | 70 | 1.25 | 87.50 | ||||||

| (14,778.50) | |||||||||

| LESS: | |||||||||

| Group classes cost | No of classes | Fees Paid to Teacher | 113 | 60.00 | (6,780.00) | ||||

| LESS: | |||||||||

| Private classes cost | No of classes | Fees Paid to Teacher | 15 | 60.00 | (900.00) | ||||

| TOTAL COSTS | (22,458.50) | ||||||||

| NET PROFIT FOR GROUP/PRIVATE/SALT CLASSES FOR THE MONTH | (10,023.50) | ||||||||

March 2013

| Main Sources of Revenue | # of client visits | Revenue per class | |||||||

| Private | 33 | 130.00 | 4,290.00 | ||||||

| Group Classes | 998 | 15.00 | 14,970.00 | ||||||

| Salt Stretch | 2 | 70.00 | 140.00 | ||||||

| TOTAL REVENUE | 19,400.00 | ||||||||

| LESS: | |||||||||

| Monthly rental | 1900 | 5.89 | 11,191.00 | ||||||

| Monthly shared administrative fees | 3,500.00 | ||||||||

| Monthly MBO fees | 70 | 1.25 | 87.50 | ||||||

| (14,778.50) | |||||||||

| LESS: | |||||||||

| Group classes cost | No of classes | Fees Paid to Teacher | 143 | 60.00 | (8,580.00) | ||||

| LESS: | |||||||||

| Private classes cost | No of classes | Fees Paid to Teacher | 33 | 60.00 | (1,980.00) | ||||

| LESS: | |||||||||

| Salt-cave classes cost – teachers | No of classes | Fees Paid to Teacher | 1 | 60.00 | (60.00) | ||||

| Salt-cave classes cost – rental | No of classes | Rental per class | 1 | 30.00 | (30.00) | ||||

| TOTAL COSTS | (25,428.50) | ||||||||

| NET PROFIT FOR GROUP/PRIVATE/SALT CLASSES FOR THE MONTH | (6,028.50) | ||||||||

April 2013

| Main Sources of Revenue | # of client visits | Revenue per class | |||||||

| Private | 10 | 130.00 | 1,300.00 | ||||||

| Group Classes | 907 | 21.00 | 19,047.00 | ||||||

| Salt Stretch | 2 | 70.00 | 140.00 | ||||||

| TOTAL REVENUE | 20,487.00 | ||||||||

| LESS: | |||||||||

| Monthly rental | 1900 | 5.89 | 11,191.00 | ||||||

| Monthly shared administrative + bus fees | 4,200.00 | ||||||||

| Monthly MBO fees | 70 | 1.25 | 87.50 | ||||||

| (15,478.50) | |||||||||

| LESS: | |||||||||

| Group classes cost | No of classes | Fees Paid to Teacher | 135 | 60.00 | (8,100.00) | ||||

| LESS: | |||||||||

| Private classes cost | No of classes | Fees Paid to Teacher | 10 | 60.00 | (600.00) | ||||

| LESS: | |||||||||

| Salt-cave classes cost – teachers | No of classes | Fees Paid to Teacher | 1 | 60.00 | (60.00) | ||||

| Salt-cave classes cost – rental | No of classes | Rental per class | 1 | 30.00 | (30.00) | ||||

| TOTAL COSTS | (24,268.50) | ||||||||

| NET PROFIT FOR GROUP/PRIVATE/SALT CLASSES FOR THE MONTH | (3,781.50) | ||||||||

May 2013

| TOTAL REVENUE | 25,188.00 | ||||||||

| LESS: | |||||||||

| Monthly rental | 1900 | 5.89 | 11,191.00 | ||||||

| Monthly shared administrative + bus fees | 4,200.00 | ||||||||

| Monthly MBO fees | 70 | 1.25 | 87.50 | ||||||

| (15,478.50) | |||||||||

| LESS: | |||||||||

| Group classes cost | No of classes | Fees Paid to Teacher | 155 | 60.00 | (9,300.00) | ||||

| LESS: | |||||||||

| Private classes cost | No of classes | Fees Paid to Teacher | 18 | 60.00 | (1,080.00) | ||||

| LESS: | |||||||||

| Salt-cave classes cost – teachers | No of classes | Fees Paid to Teacher | 6 | 60.00 | (360.00) | ||||

| Salt-cave classes cost – rental | No of classes | Rental per Class | 6 | 30.00 | (180.00) | ||||

| TOTAL COSTS | (26,398.50) | ||||||||

| NET PROFIT FOR GROUP/PRIVATE/SALT CLASSES FOR THE MONTH | (1,210.50) | ||||||||

Sheet 7

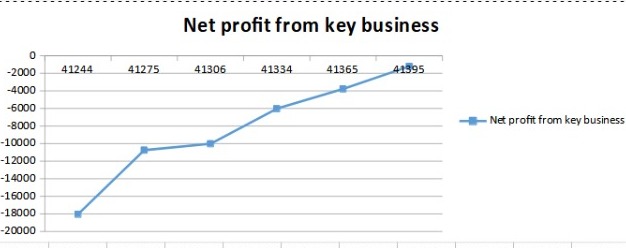

| Month | Net profit from key business |

| Dec-12 | (18,048.50) |

| Jan-13 | (10,748.50) |

| Feb-13 | (10,023.50) |

| Mar-13 | (6,028.50) |

| Apr-13 | (3,781.50) |

| May-13 | (1,210.50) |

NTU063-xls-ENG xlxs

Sheet 1

| Space & Light Studios: Cost-Volume-Profit Analysis and the Business of Yoga Teaching Note |

| Chua Wei Hwa, Koh Wei Chern & Wee Beng Geok |

| Publication No: ABCC-2014-002(TN) |

| HBP No. NTU063 |

| Break-even Analysis.xls |

| COPYRIGHT © 2015 Nanyang Technological University, Singapore. All rights reserved. No part of this publication may be copied, stored, transmitted, altered, reproduced or distributed in any form or medium whatsoever without the written consent of Nanyang Technological University. |

Break Even Analysis May 2013

| BREAKEVEN NO. OF VISITS TO GENERATE PER CLIENT | ||||||||

| TOTAL FIXED COSTS | ||||||||

| Monthly rental | Rental space – square footage 1900 | Median rent 5.89 | 11,191.00 | |||||

| Monthly shared administrative + bus fees | 4,200.00 | |||||||

| Monthly MBO fees | 70 | US$ exchange rate 1.25 | 87.50 | |||||

| Group classes cost | No of classes | Fees Paid to Teacher | From Exhibit 3 155 | 60 | 9,300.00 | |||

| TOTAL FIXED COSTS | 24,778.50 | |||||||

| AVERAGE CONTRIBUTION MARGIN PER CLIENT PER VISIT (AVERAGE REVENUE PER CLIENT VISIT PAGE 5) | $21.00 | |||||||

| Total number of client visits required for Group Classes | 1,180 | |||||||

| Number of visiting/active clients from Group Classes (PAGE 5) | 250 | |||||||

| MONTHLY NUMBER OF VISITS TO GROUP CLASSES REQUIRED OF EACH VISITING/ACTIVE CLIENT | 4.7 | |||||||

| SENSITIVITY ANALYSIS OF AVERAGE CONTRIBUTION ADJUSTED BY | -2 | |||||||

| AVERAGE CONTRIBUTION MARGIN PER CLIENT PER VISIT | $19.00 | |||||||

| Total number of client visits required | 1,304 | |||||||

| Number of visiting/active clients from Group Classes (PAGE 5) | 250 | |||||||

| MONTHLY NUMBER OF VISITS REQUIRED OF EACH VISITING/ACTIVE CLIENT | 5.2 |

NTU064-xls-ENG-xlxs

Sheet 1

| Space & Light Studios: Cost-Volume-Profit Analysis and the Business of Yoga Teaching Note |

| Chua Wei Hwa, Koh Wei Chern & Wee Beng Geok |

| Publication No: ABCC-2014-002(TN) |

| Profitability Analysis.xls |

| COPYRIGHT © 2015 Nanyang Technological University, Singapore. All rights reserved. No part of this publication may be copied, stored, transmitted, altered, reproduced or distributed in any form or medium whatsoever without the written consent of Nanyang Technological University. |

Profit By Class Type

| For May 2013 | ||||||||

| Group | Private | Salt Cave | Total | |||||

| No. of client visits (headcount) – Exhibit 4 | 1,048 | 18 | 12 | 1,078 | ||||

| Percentage | 97% | 2% | 1% | 100% | ||||

| No. of classes conducted – Exhibit 3 | 155 | 18 | 173 | |||||

| Percentage | 90% | 10% | 100% | |||||

| Revenue – Estimated from Exhibit 4 | $22,008.00 | $2,340.00 | $840.00 | $25,188.00 | ||||

| Less: | ||||||||

| Fees Paid to Teachers | $9,300.00 | $1,080.00 | $360.00 | $10,740.00 | ||||

| Rental Cost | $10,026.62 | $1,164.38 | 6 salt cave classes conducted for 12 clients. Assumed that each class had 2 clients, so rental of salt cave is $30 per session.$180.00 | $11,371.00 | ||||

| Administrative Fees | $4,168.18 | $71.59 | $47.73 | $4,287.50 | ||||

| Profit from Each Type of Class | ($1,486.80) | $24.03 | $252.27 | ($1,210.50) | ||||

| Profit Per Class Conducted | ($9.59) | $1.33 | $42.05 |

ANSWER

-

Estimate the current profit figures of SLS from December 2012 to May 2013 to evaluate the viability of the business.

Yoga has been on a rise in Singapore and it is indeed a fair assumption on the part of business owners to assume that this could be a new opportunity for making huge profits [1]. However, at the same time an increasing popularity does not mean increasing revenues of survivability. SLS was a loss-making business when it was taken over by the new owners of the company Lynn and Sumei from Verita. And even till May of 2013 it had not seen any profits in its operations [6]. The silver lining here is that the losses are actually decreasing for the company. From a loss of more than $18,000 in December 2012, the company saw a loss of merely $1210.50 in May 2013. Thus, it is reasonable to assume that the company can see a turning point soon.

The more impressive factor here is that the costs have decreased as well. Not by a huge margin but they have decreased, nonetheless. To be able to increase revenues and cut costs at the same time is an impressive feat and if continued on the same path the company should post a profit in the next month.

-

Examine SLS’s break-even point for May 2013.

The fixed and variable costs associated with such business are very high [2]. The opportunity demands high real estate investment in terms of the space for yoga and a similar investment towards trainer fees. Similar is the situation that SLS faces [5] The space rent that the company has to pay is very high and over that there is a payment of instructors and administrative expenses. Clubbed with the average contribution margin we get to a break even point of 1180 clients for group classes per month. This is a manageable number and in May 2013 SLS had a footfall of 1048 people. With an increase of about 10% it will be posting profits and meeting its breakeven. At the same time the required number of classes that every individual should attend is 4.7. Thus, if clients can be pushed to attend classes more than once a week, say both weekends then the company will be in good shape very soon.

-

Estimate the profitability of conducting each type of yoga class – i.e. group classes, private classes, and “salt cave” classes.

We have seen that the company is currently posting losses in its operations. The graph below shows where the problem with the losses lies [4]. The largest number of clients (97%) come for group classes but it has a profit margin of -6.8%. The group yoga classes saw a loss of $1486.8 in the month of May in 2013. The other two classes have seen profits, but these are not the classes where the numbers lie. The private classes account for a total of 2% of the footfall and a mere 1.03% profit margin. The profit margin is very high in Salt cave (above 30%) but as we can see that only 1% of the clients of SLS actually go come to this class. Based on the segment wise profitability we can clearly see the issues with the company and the places it needs to focus its attention on.

-

Consider the implications of the analyses above for SLS.

Based on the profitability and break-even analysis of the company and its different yoga class segments we can see that there is a lot of room for improvement in the operations of the company. The fist thing that we instantly notice is the stark difference between the usage of group packages and private packages. It implies that the current clients of SLS only see the company as a group yoga company and it might not be the choice of people who want private yoga lessons and want to personally excel in it.

If there is a new player in the market that can target the group customers of SLS then it will be in deep waters and might have to close down its operations. Regarding group packages specifically it is a loss-making venture currently and a major chunk of expenses is the fixed costs of the company which need to be reduced.

-

Conduct sensitivity analyses based on different scenarios of rental costs, fees paid to yoga teachers and pricing.

A sensitivity analysis was conducted on the break-even analysis by reducing the contribution per client by 2. Therefor the new contribution margin was $19, and we can see that the required number of client visits increased from 1180 to 1304 and the number of weekly visits increased from 4.7 to 5.2. Thus, a mere decrease of 10% in the contribution margin had a big impact on the profitability situation of the company. If this actually happens in June and stays the same, then the company might take more than a couple of months to reach its breakeven point and start posting profits. Combined with the losses it has already accumulated it might be running in problems.

-

Recommend a plan of action for the owners of SLS.

Based on the analysis that we have done for SLS we can say that the company definitely needs to make some changes in its structure on a priority. The first change that needs immediate attention is the reduction in its fixed costs [3]. The company can switch to a cheaper place in the city to save on the costs.

The second and more important change is an increase in the focus on the salt cave segment. It is a highly profitable segment and the company should focus on increasing the clients there.

Apart from that the company should also focus on marketing in general and increasing the offering from just yoga to other related segments like health foods bar.

REFERENCES

-

Singapore unveils local edition of yoga magazine. (2016). Professional Services Close – Up

-

Rao, K. R. (2017). Foundations of yoga psychology doi:10.1007/978-981-10-5409-9

-

McCall, M. C. (2014). In search of yoga: Research trends in a western medical database. International Journal of Yoga, 7(1), 4-8. doi:10.4103/0973-6131.123470

-

McCall, M. C. (2014). In search of yoga: Research trends in a western medical database. International Journal of Yoga, 7(1), 4-8. doi:10.4103/0973-6131.123470

-

Hammel, F. C., Goulet, P. G., & United States. Small Business Administration. Office of Business Development. (1989). Breakeven analysis: A decision-making tool

-

Gupta, T. (. (2012). Profitability analysis of current account portfolio. Shillong: Rajiv Gandhi Indian Institute of Management.

Looking for Finance Assignment Help. Whatsapp us at +16469488918 or chat with our chat representative showing on lower right corner or order from here. You can also take help from our Live Assignment helper for any exam or live assignment related assistance.