QUESTION

- Your assignment is to value Mercury Athletic Footwear. Remember, Mercury is a cumulative case.

- Please follow the same approach that you used to “write-up” your first case, just make sure that you solve for the discount rate using WACC.

- You should also cross-examine your final valuation using a multiples-based valuation. As you know, there are plenty of ways to do this, so just make sure that you explain the logic of your approach in your write-up.

- Finally, don’t forget to emphasize key strategic considerations with an eye on the “problem” and/or the “objective” of the case!

Case :: Mercury Athletic Footwear :Valuing the Opportunities

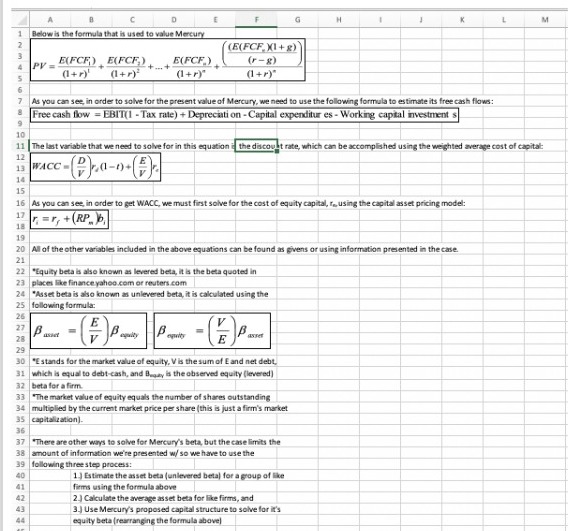

Formula use to value mercury

ANSWER

Introduction

The business heads of Active Gear Inc. have been comprehending the acquisition of Mercury Athletic Footwear for annexing their operations in the AGI brand. While AGI has a higher amount net income margin even Mercury Athletic is not far behind in terms of the net income margins. Being primarily in the Men’s footwear segment the company holds a decent command on its market due to high customer loyalty.

The company has also been able to leverage simple designs and cheap manufacturing levels by maintaining its operations. Where other companies generally focus on designs, the focus of Mercury Athletics on operations has led it to achieve some of the better margins of the industry.

At the same time there are also a few gaps that the company faces. The very first is its weak presence in the women’s footwears market. There is a long way to go for Mercury in this domain and the revenue and margins are not even comparable to what the company commands in the men’s segment. The second problem that the company faces is the high amount of days of sales in inventory. Where active gear has 42.5 days of sales in inventory, Mercury has 61.1.

Here it is important for the business heads of AGI to value the company properly to understand the risks associated with the purchase of the company.

Company Valuation by WACC

The company was previously valued using the free cash flow method but a WACC was used that was between the market range instead of the actual company WACC. We now estimate the WACC of the company based on the financials it had in 2006 as a stand-alone company.

The WACC

For the estimation of WACC we first calculate the equity beta of the company. That was done by calculation the average market asset beta and using that for the further calculations. First the asset beta of all the companies was calculated and finally the average of those asset betas was used for Mercury. The following are the calculated asset betas:

| Company | Asset Beta |

| D&B Shoe Company | 2.063758 |

| Marina Wilderness | 2.099414 |

| General Show Corp | 1.452222 |

| Kinsley Coulter Products | 0.748306 |

| Vistory Atheletics | 0.797183 |

| Surfside Footwear | 1.586425 |

| Apline Company | 0.988632 |

| Heartland Outdoor Footwear | 1.082164 |

| Templeton Athletics | 0.687049 |

| Average | 1.27835 |

The average asset beta along with the capital structure of Mercury (20% leverage) was used to calculate the equity beta of the company. Further the risk-free rate is taken equal to the terminal growth rate of 3% and the market return is taken equal to the income margin of 7.86% giving a market risk premium of 4.86%. this leads to a cost of equity value of 10.8%. Other values used are as follows:

| WACC Calculations | |

| Asset Beta | 1.27835 |

| Leverage | 20% |

| Equity/Value | 80% |

| Equity Beta | 1.597938 |

| Risk Free Rate | 3% |

| At Terminal Growth Rate | |

| Rp | 5% |

| Market Return taken at Income Margin | |

| Re | 10.8% |

| Kd | 6% |

| Tax | 40% |

| Kd(1-T) | 3.60% |

The WACC was hence calculated to be 9.33%.

Company Value

Based on the WACC the following are the valuation calculation:

| Free Cash Flow to Firm | 21237 | 26727 | 22096 | 25472 | 29543 |

| Terminal Value | 480504.2669 | ||||

| Total Cash Flow | 21237 | 26727 | 22096 | 25472 | 510047.2669 |

| Present Value | $402998 |

Based on the fact that there might be further possible synergies with AGI it was estimated that Mercury will be able to revive the Women’s casuals’ brand where the revenues will grow with the market revenue CAGR whereas the operating expenses will stay the same. Based on that the optimistic value of the company is as follows:

| Free Cash Flow to Firm | 21237 | 28590.794 | 26309.858 | 32262.78025 | 39162.40693 |

| Terminal Value | 636959.8089 | ||||

| Total Cash Flow | 21237 | 28590.794 | 26309.858 | 32262.78025 | 676122.2158 |

| Present Value | $518838 |

The value of the company will increase by more than 25% if Mercury is able to revive its women’s brand and acquiring the company for the base case valuation will then prove to be very profitable investment for the company.

Company Valuation by Multiples Method

Before accepting the valuation of the company, it is important for the business heads to verify the valuation with the comparable multiples’ method. In this method valuation the average valuation multiple is used to find the company value. For valuing Mercury, four valuation multiples have been chosen, EBIT multiple, EBIDTA multiple, Price to earnings multiple and book to value multiple. In all four multiples we multiply the industry average multiple with relevant company financial from the year 2006. The company values hence reached are as follows:

| Multiples Valuation | ||

| EBIT Multiple | ||

| Industry Average | 10.48 | |

| Company EBIT | $ 42,299.00 | |

| Company Value | $ 4,43,199.52 | |

| EBIDTA Multiple | ||

| Industry Average | 8.96 | |

| Company EBIT | $ 51,804.00 | |

| Company Value | $ 4,63,933.60 | |

| P/E Multiple | ||

| Industry Average | 13.81 | |

| Company EBIT | $ 25,998.00 | |

| Company Value | $ 3,59,061.27 | |

| B/V Multiple | ||

| Industry Average | 2.54 | |

| Company EBIT | $ 2,14,067.00 | |

| Company Value | $ 5,44,681.59 | |

| Average Company Value | $ 4,52,718.99 | |

We can see that the range of company valuation from the comparable multiples’ method is from $ 3,59,061.27 to $ 5,44,681.59. The average company value of $ 4,52,718.99 is very close to the valuation that we received from the WACC valuation method and much below the valuation that 8% of discount rate gave us. Thus, the calculation using the WACC seem to be appropriate and should be accepted going further.

Strategic Considerations

Based on the valuation of the company is seems to be a good investment but AGI has to prepare for the strategic gaps that exist with Mercury currently. The primary advantage that both the companies and specially AGI will gain is the consolidation of resources. Both the companies excel in a few things. Mercury has a brilliant distribution channel that will be leveraged by AGI and thus, this will lead to a decrease in costs and increase in the margins for the new bigger company.

At the same time AGI is better at inventory management which will help Mercury reduce its days of sales in inventory and increase its margins. The companies will also not cannibalise much of each other’s markets as they have a separate target customer group.

Looking for best Finance Assignment Help. Whatsapp us at +16469488918 or chat with our chat representative showing on lower right corner or order from here. You can also take help from our Live Assignment helper for any exam or live assignment related assistance